There’s a lot to unpack in the real estate market right now, but for potential homebuyers, the coming months could be an exciting time. Let’s dive into two key trends that are pointing towards a more favorable market for buyers.

Inflation and Mortgage Rate Outlook

First, there’s some positive news on the inflation front for mortgage rates. The most recent CPI inflation report showed that inflation decreased on a month-over-month basis, which was the first time since 2020. This is a significant development, as inflation has been a major driver of rising interest rates over the last few years. A continued dip in inflation is likely paving the way for a rate cut by the Federal Open Market Committee (FOMC) to the Fed Funds Rate later this fall. In fact, the markets are currently pricing in a probability of over 90% that we will see a rate cut following the September FOMC meeting, which will help bring down mortgage rates. This will help make homeownership more affordable and bring about refinancing opportunities for current homeowners.

Housing Inventory Increasing

On the housing market side, we continue to see inventory build for both existing and newly constructed homes. Although lower mortgage rates will allow for more buyers to enter the market, more homes also mean more options for you to find your perfect fit. Whether you’re looking for a cozy starter home or a spacious family residence, the growing inventory expands your choices and reduces the pressure often felt in a low inventory market.

What does this mean for homebuyers?

If you’ve been thinking about buying a home, these trends could be a sign that the time is right. With potentially lower mortgage rates and a shift in the housing market, you may be able to find a great home at a good price.

Here are some steps you can take to get ahead of the curve:

Get pre-approved for a mortgage. This will give you a clear understanding of how much you can afford to borrow and make you a more competitive buyer.

Start your house hunt early. With a potential for lower rates in the future, the sooner you start looking, the better chance you’ll have of finding your dream home before competition increases.

Work with a real estate agent. A real estate agent professional can help you navigate the buying process, negotiate offers, and find the right home for your needs.

The housing market may be shifting, but with the right preparation and a little guidance, you can turn this shift into an opportunity to achieve your homeownership goals. Let’s get you started on your journey today!

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

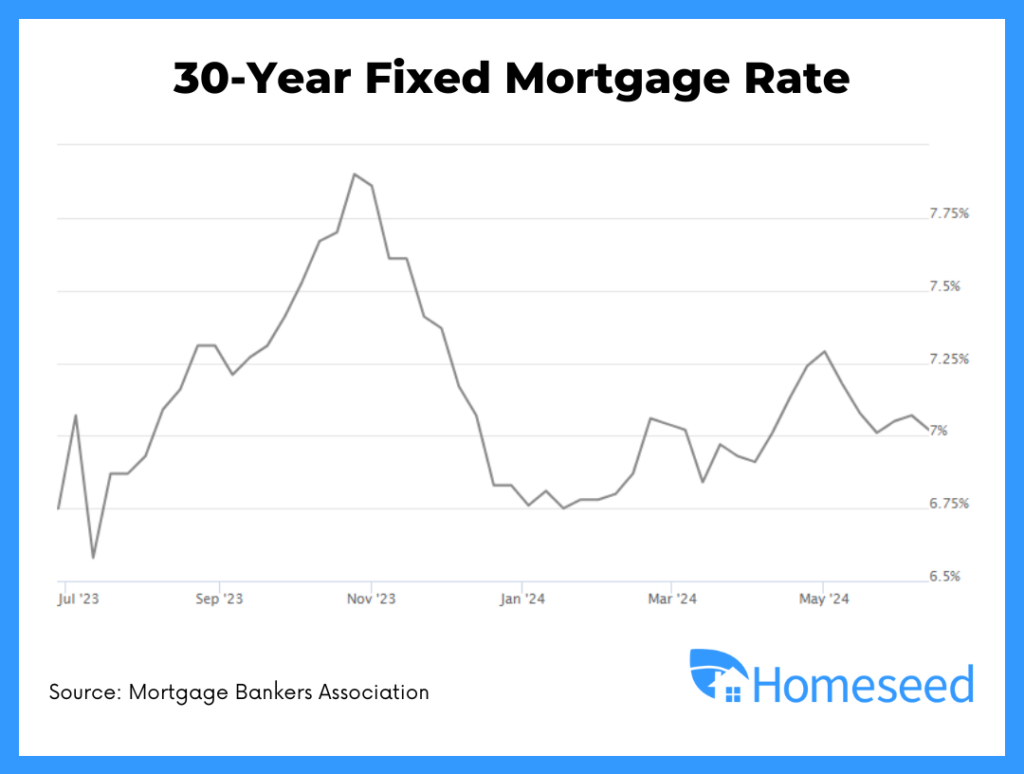

Mortgage rates are slightly lower on a week-over-week basis and have been fluctuating within a narrow range over the last month.

Expectations are for tomorrow’s CPI report to show year-over-year inflation decreasing from 3.3% to 3.1%, which would be good for mortgage rates.

Market futures are showing two potential rate cuts by the end of 2024 as having the highest probability.

Consumer Price Index

Headline inflation fell from 3.3% to 3.0% year-over-year,

June CPI showed a large moderation in the shelter component.

There is a long lag in reflecting real world market conditions, but we continue this trend in shelter inflation lowering.

BLS Jobs Report

June’s job growth was slightly above estimates with a reported 206,000 new jobs created.

However, there were big revisions to the two previous months with a combined 111K jobs removed.

Unemployment also rose to 4.1%, which triggered a reliable economic indicator suggesting we are already in a recession.

Digging Deeper on Housing Inventory and Prices

Active inventory has risen 6.7% in June and is up 37% year-over-year, but this is from very low numbers with one third of the increase coming from two states alone – Florida and Texas.

On the moderation of median home prices, this is skewed by the mix of sales (lower priced homes are selling more than higher priced homes), which brings down the median price sold.

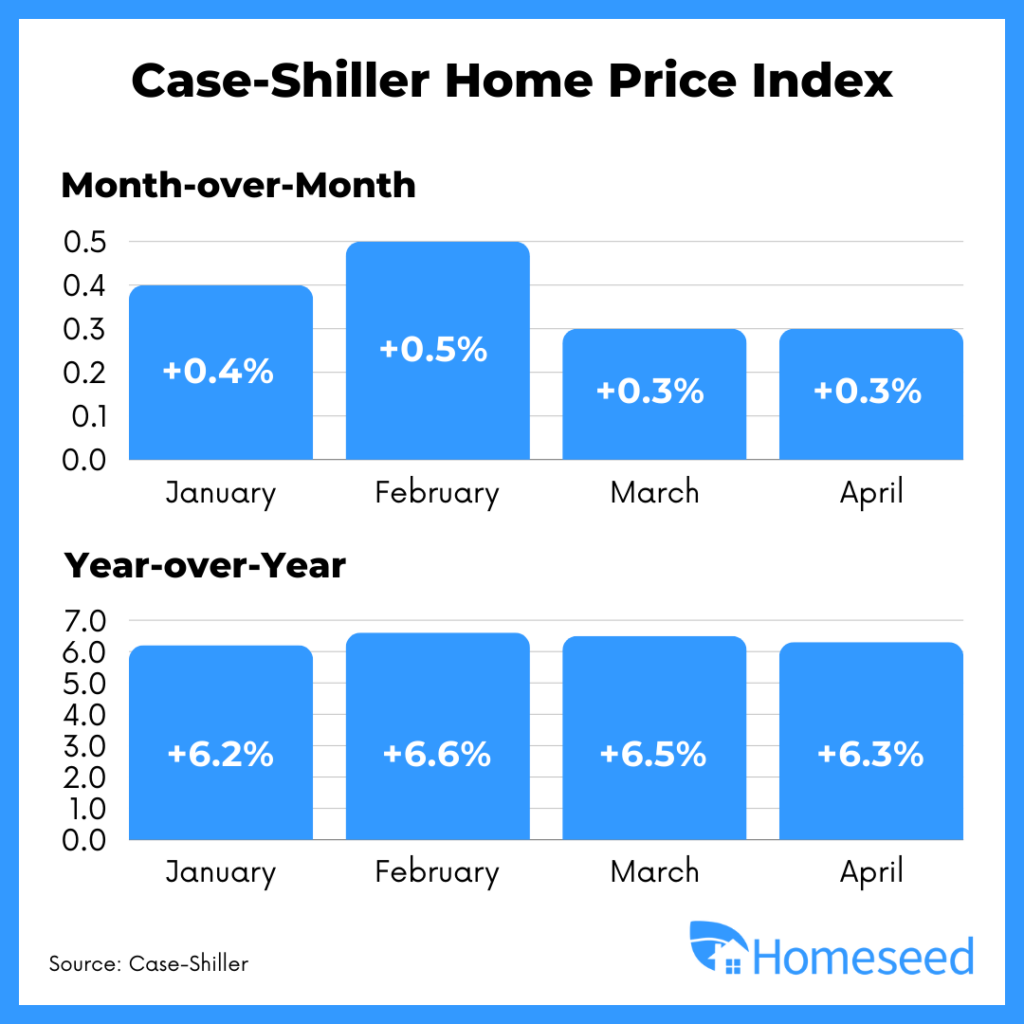

Home values across the board are increasing as shown in the recent Case-Shiller Home Price Index and inventory remains much lower than pre-pandemic levels.

RATES EDGE SLIGHTLY UNDER 7% – Mortgage rates average just under 7% for top tier scenarios according to this index. https://www.mortgagenewsdaily.com/…

WHEN WILL RATE CUTS COME – The Fed says it needs greater confidence inflation is moving towards its 2% goal before they will cut rates. https://www.cnbc.com/…

AFFORDABILITY CHALLENGES – How getting inflation back towards the Fed’s 2% target will help housing. https://www.housingwire.com/…

Homeowners across the country are experiencing unprecedented levels of home equity as home values continue to rise. This surge presents a unique opportunity to leverage that equity through a cash-out refinance. In this blog post, we’ll explore what a cash-out refinance is, how it works, and how it can be a strategic move for consolidating debt and funding significant investments or projects.

What is a Cash-Out Refinance?

A cash-out refinance is a financial transaction in which you replace your existing mortgage with a new one that’s larger than what you currently owe. The difference between the new loan amount and the existing mortgage balance is paid out to you in cash. Here’s a simple breakdown of how it works:

Appraisal: Your home’s value is assessed to determine how much equity you have.

New Mortgage: You take out a new mortgage for more than you owe on your current one, limited up to 80% of the current appraised value.

Cash Payment: You receive the difference in cash, which can be used for a variety of purposes.

Consolidating Your Debts

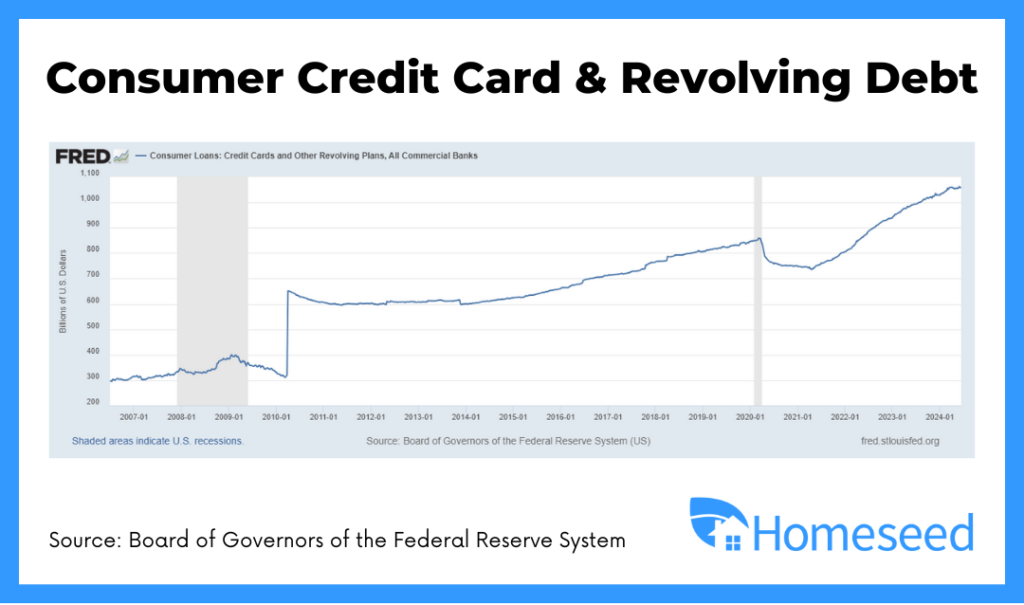

Alongside rising home equity, debt levels have also reached new heights. Many homeowners carry high-interest debt from credit cards, personal loans, or other sources. A cash-out refinance can be an effective tool for consolidating this debt. By using the cash from the refinance to pay off high-interest debts, you can lower your overall monthly payments and improve your cash flow.

Lowering Your Blended Interest Rate

One of the key considerations in deciding whether to pursue a cash-out refinance is the interest rates involved. Even if your current mortgage rate is lower than the rate you would get with a cash-out refinance, your overall blended interest rate—taking into account all your debts—could be lower. This means you could save money in the long run by consolidating high-interest debts into a single, more manageable payment.

Fundings for Projects or Investments

Home Improvement Projects: Invest in renovations or upgrades that can increase your home’s value even further.

Purchasing a Second Home: Use the cash to make a down payment on a vacation home or rental property.

Other Investments: Allocate funds towards other investment opportunities that can potentially yield higher returns.

Learn More About Your Options

With home equity at an all-time high and debt levels rising, a cash-out refinance offers a strategic way to manage finances, reduce debt, and fund important projects or investments. By understanding how it works and considering your financial goals, you can make informed decisions that maximize the benefits of your home’s value.

If you’re considering a cash-out refinance, contact Homeseed today to discuss your options and see how we can help you achieve your financial objectives.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are higher week-over-week despite lower inflation from the PCE report last Friday, along with weaker manufacturing data from today.

Market experts believe that bonds, which drive mortgage rates, are are reacting to concerns about a potential GOP sweep in the government, which could have negative implications for Treasury supply.

Looking ahead, we might see increased rate volatility during this election year as we approach the end of 2024.

Home Values Continue to Increase

Two of the most notable home price indices, Case-Shiller and FHFA, show that home values continue to rise on a year-over-year basis in their most recent reports.

Both Case-Shiller and FHFA reported year-over-year gains of 6.3%.

Strong demand and tight supply will likely push home values higher and allow homeowners to build wealth through equity.

Existing Home Sales

Inventory increased 6.7% month-over-month in May 2024 and is up 18.5% year-over-year.

Homes were on the market for a national average of 24 days.

Given the demand and low inventory, 30% of homes sold above the list price.

RATES MOVE HIGHER – Concerns over a potential sweep by the GOP in the upcoming elections could have negative implications for Treasury supply, which have driven up mortgage rates. https://www.mortgagenewsdaily.com/…

PERSONAL CONSUMPTION EXPENDITURES – Tomorrow’s PCE report is expected to show the lowest core reading since March 2021. https://www.cnbc.com/…

USING AI FOR APPRAISALS – The CFPB approved a new rule that aims to govern how AI is used to estimate the value of a home. https://www.housingwire.com/…

WHEN WILL HOME PRICES GO DOWN – Six economists weigh in on the likelihood of home prices going down. https://www.morningstar.com/…

Welcome to Homeseed’s Summer Market Update for 2024! As we reach the halfway point of the year, it’s essential to reflect on the trends and developments that have shaped the mortgage market and housing industry thus far. The first six months of 2024 have been characterized by fluctuating mortgage rates, evolving economic conditions, and dynamic shifts in buyer behavior. Let’s dive into the key insights and projections that will guide us through the remainder of 2024.

Factors Influencing Mortgage Rates

Federal Reserve:

Controls short-term interest rates that indirectly impacting mortgage rates.

As a general rule of thumb, rates rise in a strong economy and fall when the economy slows.

Inflation:

Bond Market: Inflation can reduce investor demand for mortgage-backed securities, which then causes bond prices to fall and mortgage rates to increase.

Devaluation of Dollar: As inflation increases, the purchasing power of the dollar decreases, which can lead to higher prices for everything, including mortgage rates.

Monthly Jobs Report:

Strong employment and wages can put upward pressure on inflation.

Weak employment data and rising unemployment will lead to rate cuts in an attempt to jumpstart the economy.

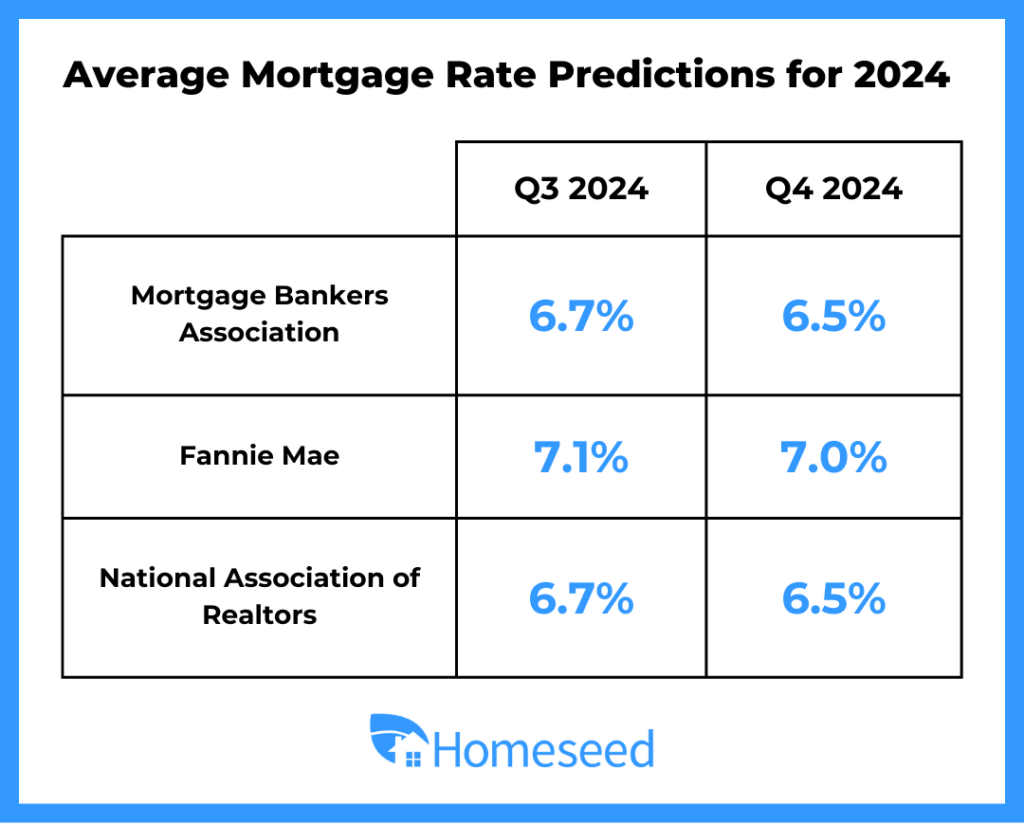

Mortgage Rate Outlook & Predictions

Initial 2024 Predictions:

Early 2024 predictions included three rate cuts by the Fed, which lead many experts in the industry to predict mortgage rates would fall in to the low 6% range by the end of the year.

Concerns that the Fed would keep rates higher for longer began to arise in the first quarter of 2024 due to stalled progress on getting inflation towards their 2% goal.

Recent FOMC Meeting:

Median expectation by Fed members now shows only one potential rate cut in 2024.

Recent economic data has shown softening inflation and labor market, leading to lower rates over the past two months.

Future Rate Trends:

Most forecasts expect mortgage rates to fall slightly towards the end of 2024 to a range of 6.5% – 6.75%.

Significant drops in inflation and rising unemployment could lead to faster rate decreases.

Key reports influencing rates: BLS Jobs Report and Consumer Price Index (CPI).

Chance of increased volatility in rates as we near the presidential election due to any potential uncertainty that may come about.

Housing Market Update

Inventory and Supply:

Inventory up nearly 35% from 2023, but still well below historical supply prior to the pandemic.

Current inventory at 3.7 months’ supply compared to what is considered a balanced market at 6 months supply.

Home Values & Demand:

Home values will likely continue to increase through the end of 2024 as demand outweighs supply.

Mortgage application volume for purchases have increased for three consecutive weeks and are at the highest level since January 2024.

Consumer Debt & Home Equity

Record High Consumer Debt:

Consumer debt reached $1.15 trillion in Q1 2024.

High credit card debt, rising charge-offs, and delinquencies suggest a potential slowdown in consumer spending.

Impact on Economy:

Reduced consumer spending could lower inflation and slow the economy, benefiting mortgage rates.

Homeowners with high equity and debt could benefit from cash-out refinancing to improve cash flow.

Opportunities This Summer

The summer market is brimming with opportunities for both homeowners and homebuyers. With potential mortgage rate adjustments expected later this year, an estimated 5 million buyers could enter the market for every 1% drop in rates. Alongside the expanding inventory, this is the perfect time to stay informed and make strategic financial decisions. Whether you’re looking to upgrade your current home or start your homeownership journey, reach out today to explore the opportunities available this summer.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

It’s been a volatile week for rates as they are now slightly lower than where they were a week ago.

A strong BLS Jobs Report earlier in the month moved rates higher before last week’s CPI report brought them back down.

Last Thursday’s Producer Price Index helped rates move even lower as inflation measured from the perspective of manufacturers came in much lower than expected.

Consumer Price Index (CPI)

The May CPI report showed that overall inflation was flat at 0% month-over-month (expected 0.1%) and decreased year-over-year from 3.4% to 3.3%.

May brought cooler than expected consumer inflation, due in large part to easing motor vehicle insurance costs.

This follows better than expected readings in April as the annual Headline and Core readings both took important steps lower.

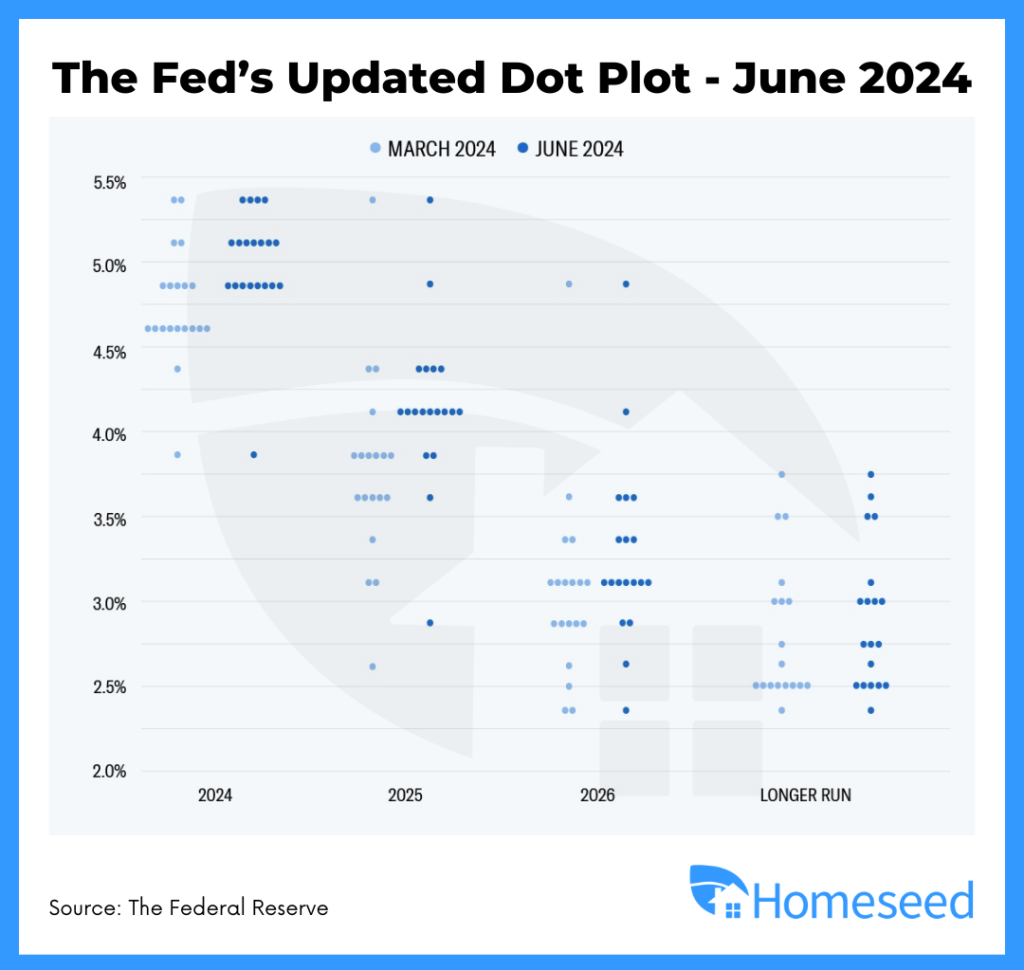

The Fed Meeting

The Fed’s fourth meeting of the year concluded last Wednesday and left their Fed Funds Rate unchanged once again.

An updated dot plot showed that the median forecast for the rest of the year would be one rate cut.

Fed Chair Jerome Powell acknowledged that their policy is restrictive but needs to see more progress on inflation lowering.

RATES DROP AFTER CPI DATA – Lower inflation numbers help bring rates back down after last week’s spike from the BLS jobs data. https://www.mortgagenewsdaily.com/…

WHOLESALE PRICES COME DOWN – The Producer Price Index (PPI), a gauge of prices that producers get for their goods and services, declined 0.2% for the month. https://www.cnbc.com/…

MORTGAGE APPLICATIONS RISE IN MAY – New-home purchase mortgage applications rose 1% month-over-month in May according to the Mortgage Bankers Association (MBA). https://www.housingwire.com/…

VA NOW ALLOWING BUYER-PAID BROKER FEES – Veterans using VA home loan benefits will have the ability to pay the buyer-broker fee beginning August 10, 2024. https://news.va.gov/…

Purchasing a home is a significant, exciting milestone that can help you build generational wealth. Whether you’re a first-time homebuyer or looking to upgrade, achieving this dream is possible, but there are several hurdles to navigate in today’s housing market. Limited housing supply and ongoing affordability challenges are common obstacles that potential homeowners must overcome. In this blog, we’ll explore various challenges that homebuyers are facing in today’s market and provide housing hacks and financing strategies to help you overcome these common challenges.

1. Buy Before You Sell

One of the biggest dilemmas for homeowners looking to upgrade is buying a new home before selling their current one. Our “Buy Before You Sell” program addresses this by allowing you to make a non-contingent offer on a new home before selling your existing property.

How It Works:

You receive financial backing to purchase your new home without needing to sell your current one first.

This enables you to make a stronger, non-contingent offer, which is often more attractive to sellers.

Benefits:

Avoid the stress of timing two transactions perfectly.

Have the comfort of moving into your new home before dealing with the sale of your old one.

2. Down Payment Assistance

Saving for a down payment can be a daunting task, especially if you have limited savings. Or perhaps you want to keep some of your savings to furnish your home after closing. Fortunately, our Homeseed 100 Program is available to help with down payments and reducing your cash-to-close, even if you’re not a first-time homebuyer. We also offer down payment assistance through the Washington State Housing Finance Commission, where there are additional programs with income restrictions that could be potentially better suited for underserved and low-income communities.

Homeseed 100 Program Highlights:

No income restrictions.

Minimum credit score of 620.

Repayable and non-repayable assistance

Up to 5% assistance for the down payment and closing costs.

Manufactured homes allowed.

2-1 interest rate buydowns available.

3. Stronger Offers with a Cash Committed Credit Approval

Homeseed’s goal is to reduce the stress of the mortgage process by helping our clients prepare early and make our clients’ offers stand out in a competitive market. To do so, we’ve developed our Cash Committed Credit Approval™ program to help achieve this. We’ll provide you with a fully underwritten credit approval for financing before you find your home so you can shop with confidence. Additionally, sellers will find your offer that much more attractive knowing that you’ll close on time or our Cash Committed Credit Approval™ program will issue a $10,000 credit to them. Please see full terms and conditions at bit.ly/homeseedccc.

How It Works:

Complete a loan application and request to enroll in our Cash Committed Credit Approval program prior to making an offer.

Respond to all of our requests on time as outlined in our terms and conditions.

We will guarantee the transaction closes on time or we will issue $10,000 to the seller.

4. Multi-Family Property Purchase

Purchasing a multi-family property offers numerous benefits, making it an attractive investment option. One of the key advantages is that potential rental income from the other units can be used when qualifying for the mortgage. For individuals looking to get into real estate investing, purchasing a multi-family property provides an opportunity to build wealth and financial stability as you live in one unit and rent out the others to offset living expenses.

Scenario: Imagine Jane, an aspiring real estate investor, decides to purchase a duplex for $800,000. She secures a mortgage with a 20% down payment of $160,000, leaving her with a loan of $640,000 at a 6% interest rate. Sarah plans to live in one unit while renting out the other.

The rental market in her area is strong, and she finds a tenant who agrees to rent the second unit for $2,000 per month. The monthly mortgage payment for her loan, including principal and interest, is approximately $3,837. Adding property taxes and insurance, her total monthly housing cost comes to about $4,500.

With the rental income of $2,000 per month, Sarah’s out-of-pocket expense for housing is reduced to $2,500 per month. This makes homeownership more affordable for her. Additionally, Sarah benefits from potential property appreciation and tax advantages such as deductions for mortgage interest, property taxes, and depreciation on the rental unit. By renting out the second unit, Sarah not only reduces her living costs but also builds equity in the property, paving the way for future investment opportunities and financial growth.

5. Funds for Investing: HELOCs

A Home Equity Line of Credit (HELOC) offers significant benefits, particularly if you are looking for a quick way to tap into your home’s equity. It provides flexible access to funds by leveraging the equity built up in your current home, allowing for the financing of a new home purchase or another investment. This flexibility can ease the stress of timing for your particular goals, offering funds that cover down payments, renovations, and much more.

HELOC Highlights:

A flexible credit line secured by your home’s equity and allows for periodic access to funds when needed.

Adjustable interest rates, providing flexibility but requiring careful financial planning.

6. Utilizing a Rent-Back Agreement When Selling

A Rent-Back agreement allows the seller to remain in the home for a specified period, paying rent to the new homeowner. It provides the seller with additional time to secure a new residence and complete their move, potentially saving time and money as they would not need to move into new temporary housing before purchasing a new home.

Scenario: Imagine John just closed the sale of their home in Seattle but needs an additional 30 days to finalize the purchase of a new property. He enters into a rent-back agreement with the buyer, agreeing to pay a monthly rent equivalent to the new homeowner’s mortgage payment, property taxes, and insurance costs. The terms are clearly outlined in a written agreement, including a refundable deposit to cover any potential damages. The buyer, now the official homeowner and temporary landlord, benefits from an additional rental income that can help offset moving and closing costs. Meanwhile, the seller enjoys the stability of remaining in their home while they transition to their new one, avoiding the inconvenience and expense of temporary housing.

Get In Touch With Your Homeseed Loan Advisor

Your Homeseed Loan Advisor is here to offer innovative solutions to common homebuying obstacles, making your path to homeownership more accessible and manageable. By leveraging strategies such as Buy Before You Sell, down payment assistance, cash committed credit approvals, HELOCs, and other creative financing ideas, you can navigate the challenges of today’s real estate market with confidence. Explore these options to take control of your homebuying journey and turn your homeownership dreams into reality.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates moved higher in the early half of last week, but have since moved back down.

April’s Personal Consumption Expenditures (PCE) report was released last Friday, which showed inflation slightly below expectations and helped rates move lower.

Today’s weaker manufacturing data further supported the decrease in rates and we essentially back to where we were for rates about a week ago.

Personal Consumptions Expenditure

The Fed’s favored inflation measure, Core PCE, rose 0.2% from March to April, coming in slightly below estimates.

On an annual basis, Core PCE remained at 2.8% for the 12 months ending in April.

While this is well below 2022’s 5.6% peak, progress toward the Fed’s 2% inflation target remains stalled.

All-Time High for Home Values

Two of the most notable home price indices, Case-Shiller and FHFA, show that home values continue to rise on a year-over-year basis in their most recent reports for the end of March 2024.

Case-Shiller reports that home prices rose 6.5% year-over-year while FHFA reported a year-over-year gain of 6.6%.

Strong demand and tight supply will continue to push home values higher and help homeowners build wealth through equity.

ERASING LAST WEEK’S SPIKE – Lower inflation and weaker manufacturing data helped rates return back to where they were about a week ago. https://www.mortgagenewsdaily.com/…

MOST HOMES FOR SALE SINCE JULY 2020 – Recent data shows that active inventory and new listings are up significantly year-over-year. https://www.calculatedriskblog.com/…

TURNING CAUTIOUS ON SPENDING – Consumers and businesses are slowing down on the rate of purchases made according to banking data. https://www.cnbc.com/…

CFPB REVIEWING JUNK FEES – The Consumer Financial Protection Bureau (CFPB) is assessing how “junk fees” directly impact the health of consumers. https://www.housingwire.com/…

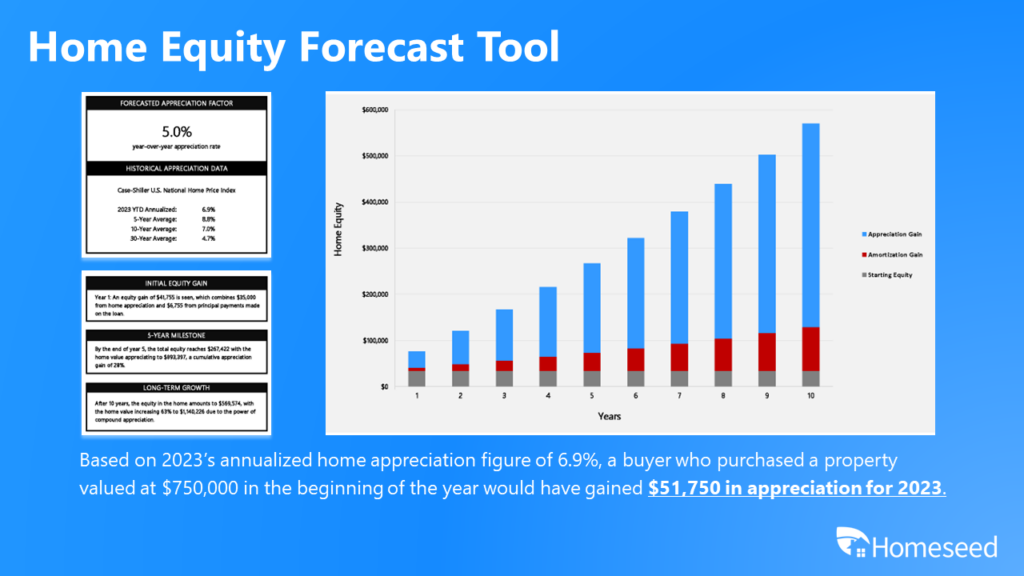

Investing in real estate has long been considered a smart move for building wealth. Two key reasons for this are the steady home appreciation and the ability to leverage your initial investment. In this blog post, we’ll explore these concepts in detail, showing why real estate remains one of the top ways to build wealth.

Understanding Home Appreciation

Home appreciation refers to the increase in a property’s value over time. Historically, real estate has shown a steady trend of appreciation, making it a reliable long-term investment. Looking at data from the US Census Bureau, homes have appreciated at about 5% annually in the US for the last 40 years.

In our current housing market, demand from homebuyers surpasses the supply in inventory, which have been supportive of home prices and are this trend is expected to keep home values appreciating in the future. At the end of Q1 2024, home prices appreciated by 6.6% year-over-year in the US with the breakdown by state you can see in the chart below.

Lastly, a recent Home Price Expectation Survey by Fannie Mae, which polled over 100 housing experts across the industry, projects an expected increase in home values by 20.8% from Q1 2024 to Q4 2028. This means a home purchased for $750,000 at the beginning of 2024 is expected to rise in value to $906,000 by the end of 2028.

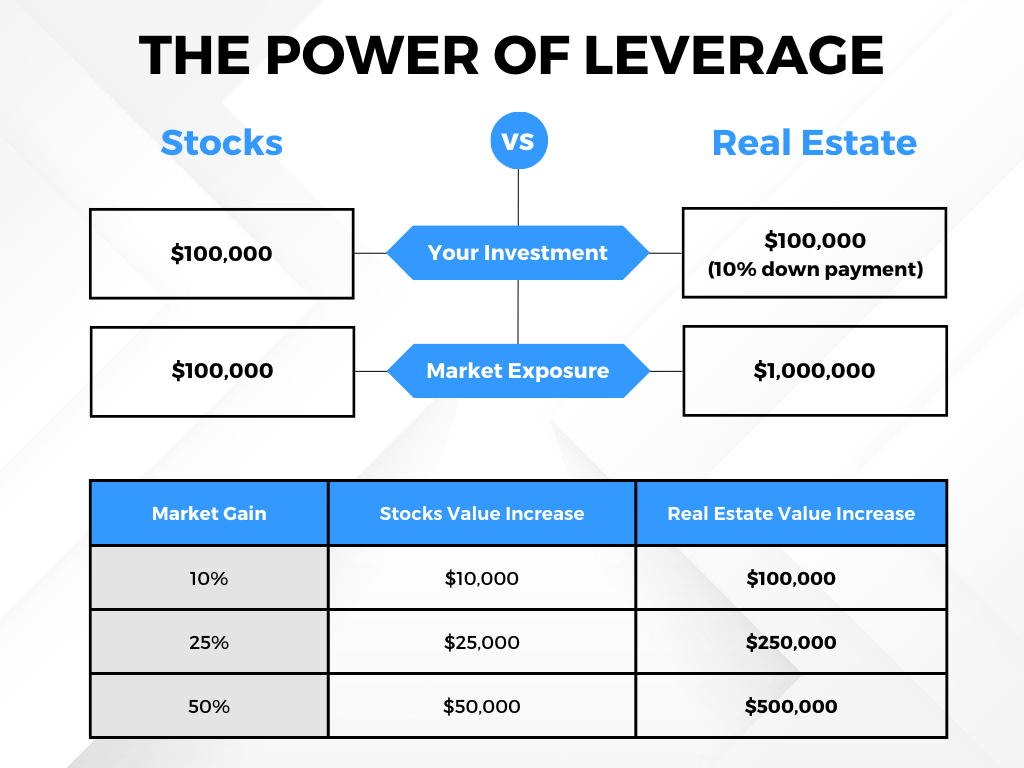

The Power of Leverage in Real Estate Investment

When you purchase a home, you typically provide a down payment and pay closing costs, while the rest of the purchase price is financed through a mortgage. This means you control an asset’s full value with your initial payment, which is considered a form of leverage. As the property appreciates, the return on your investment is calculated based on the property’s entire value and its market exposure, not just your down payment. If we compare this scenario to investing in the stock market, we can see the power of leverage even though the S&P 500 has provided a higher average annual rate of return at about 10%. This leverage magnifies the potential for wealth accumulation through real estate.

Example:

Purchase price: $750,000

Down payment: 5% ($37,500)

Closing costs: $7,500

Total Initial Investment: $45,000

With this initial investment of $45,000, you gain control of a $750,000 asset.

Real Estate Gain:

Total Initial Investment: $45,000 (down payment and closing costs)

Value of Home When Purchased: $750,000

Average Annual Rate of Appreciation: 5% (Home Values Last 40 Years)

After 5 years, the Home Value Increases to: $957,211

5-year Gain in Value: $207,211

Return on Investment (ROI): 460%

Stock Market Gain:

Total Initial Investment: $45,000

Value of Stock When Purchased: $45,000

Average Annual Rate of Return: 10% (S&P 500 Last 30 Years)

After 5 Years, the Stock Value Increases to : $72,473

5-year Gain in Value: $27,473

Return on Investment (ROI): 61%

Homeseed Can Help You Get Started

Discover the possibility of owning a home and investing in real estate with some of our exclusive loan programs that require little to no down payment. This means you can potentially start building equity and wealth with very little upfront investment. Our commitment is to make homeownership accessible and financially advantageous for you. Contact us today to discuss your goals, explore available opportunities, and make informed decisions about your real estate investment.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates have been on a consistent downward trend the last two weeks due to weakening economic data from reports such as the BLS Jobs Report, CPI, and Retail Sales.

With the weaker data, the financial markets are now expecting two rate cuts from the Fed this year.

The next market moving data will likely be the Personal Consumption Expenditures (PCE) report at the end of the month, which is the Fed’s favorite measure of inflation.

Consumer Price Index (CPI)

The Consumer Price Index continues to be the biggest source of momentum for mortgage rates as it measures inflation.

The April report released today showed overall inflation rose 0.3% for the month versus the expected 0.4%, while year-over-year inflation decreased from 3.4% to 3.5%.

Much of the core rate, which excludes food and energy, is coming from motor vehicle insurance (+22.6% YoY) and shelter (+5.7% YoY).

New Home Construction

Housing starts rebounded in April, rising 5.7% from March.

Building permits, which represent future construction, declined.

Completions did rise in April, but the numbers were a bit softer than expected and could limit much-needed supply down the road.

RATES ON A DOWNWARD TREND – Mortgage rates have consistently moved lower the last two weeks after multiple reports showing weakness in the economy. https://www.mortgagenewsdaily.com/…

INFLATION EASES IN APRIL – Today’s CPI report showed inflation in line with expectations and the lowest 12-month core reading since April 2021. https://www.cnbc.com/…

UNLOCKING MORE HOME EQUITY – Freddie Mac, one of the US’s government-sponsored enterprises, is proposing that it be allowed begin purchasing home equity loans which would help unlock equity for homeowners. https://www.businessinsider.com/…

INVESTMENT FROM HUD – The US Department of Housing and Urban Development (HUD) announced it has secured approval for $1.1 billion in funding to help with tribal housing and community development. https://www.housingwire.com/…

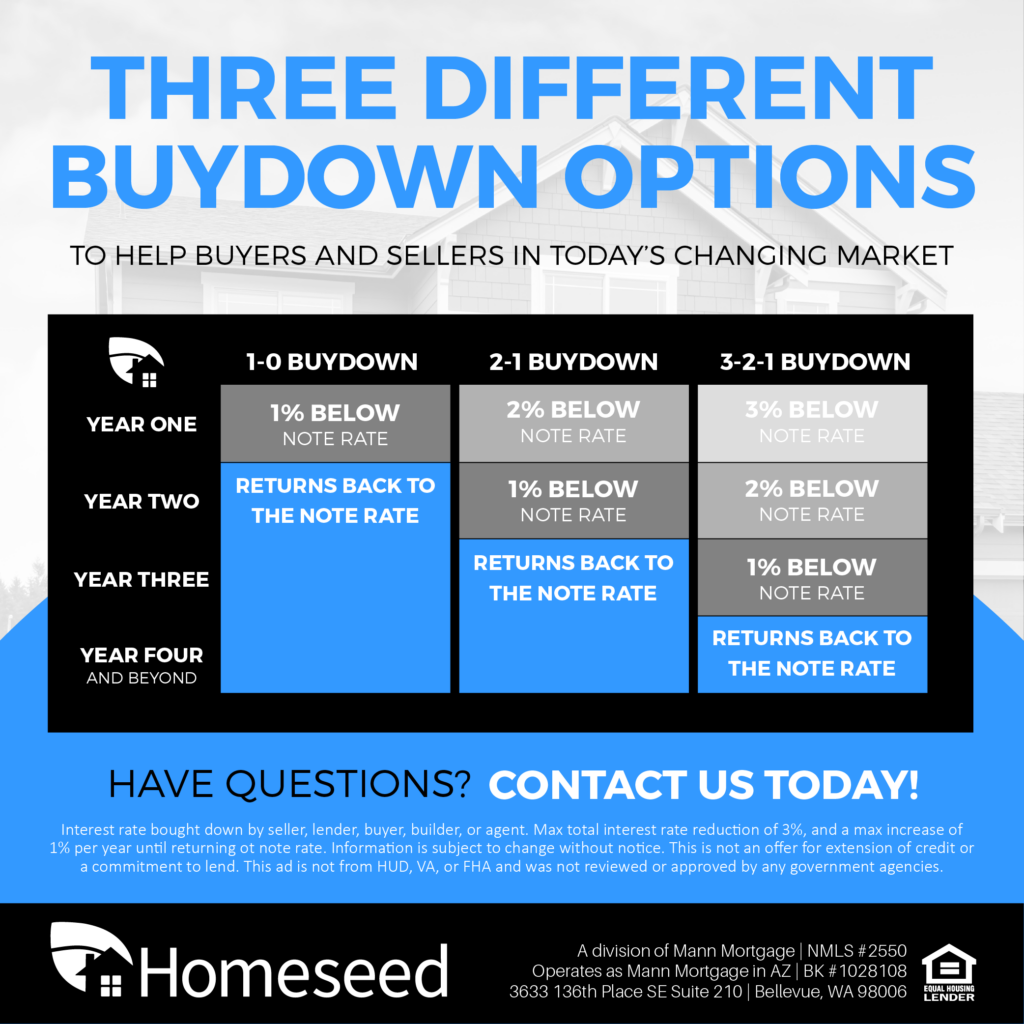

In today’s real estate market, the landscape may seem daunting to would-be homebuyers. Elevated interest rates, coupled with negative media speculation, have cast a shadow of doubt over the feasibility of homeownership. However, amidst these challenges lies a strategy that could help you become a homeowner: interest rate buydowns. We’ll explain how this strategic tool can empower you achieve homeownership and begin building wealth through real estate.

Understanding Interest Rate Buydowns

Interest rate buydowns offer a strategic approach to securing a lower interest rate, thereby reducing monthly payments and long-term borrowing costs. At Homeseed, we provide both temporary and permanent buydown options tailored to meet your unique financial goals and circumstances. Clients can also combine the benefits of both temporary and permanent buydowns to lower their monthly payment even more.

Temporary Buydowns: A Gradual Path to Affordability

Temporary buydowns are financing options that allow borrowers to lower their initial mortgage interest rates, which gradually increase over a specified period. The four most common types of temporary buydowns offered by Homeseed are the 1-0 buydown, 1-1 buydown, 2-1 buydown, and 3-2-1 buydown. This gradual approach allows you to ease into homeownership, mitigating financial strain and providing breathing room to adjust to your new responsibilities. Additionally, any unused financing credit put towards the temporary buydown will be applied to your principal loan balance if you refinance before the buydown period is over.

Permanent Buydowns: Securing Long-Term Savings

For those seeking lasting benefits, permanent buydowns offer a compelling solution. By purchasing discount points upfront, you can permanently lower your interest rate for the entire loan term. While this requires an initial investment upfront with no possibility of a refund when refinancing, the long-term savings and financial flexibility it provides can be significant, especially for buyers needing a lower monthly payment in order to qualify for the loan. Payment towards a permanent buydown can also potentially help lower your taxable income when filing taxes.

A Comparison Between Temporary and Permanent Buydowns

Leveraging Seller Concessions

In some situations with today’s market, sellers can be motivated to offer seller concessions toward closing costs, including fees associated with buydowns, to further enhance the attractiveness of purchasing their home. By leveraging these concessions, buyers can minimize their out of pocket expenses and expedite their path to homeownership.

Conclusion

Despite the noise surrounding the real estate market, interest rate buydowns stand as a highly useful strategy for aspiring homeowners. Whether opting for a temporary or permanent solution, the benefits are clear: increased affordability, financial flexibility, and long-term savings. With the support of a Homeseed Loan Advisor, you can confidently navigate the complexities of the current real estate landscape and embark on the journey to homeownership with optimism and assurance.

Welcome to Homeseed’s 2024 Spring Market Update! We are in the thick of the spring market and there have been many promising shifts in the real estate and mortgage markets recently. Whether you’re a seasoned homeowner or a hopeful buyer, the current market presents ample opportunities worth exploring. Let’s delve into the latest trends shaping the spring market and what they mean for you.

Mortgage Rate Outlook

The trajectory of mortgage rates has been a focal point for many, and recent developments shed light on what lies ahead. Since the outset of the year, rates have shown an upward trend, influenced by factors such as inflation dynamics and the strength of the labor market. While initial projections hinted at multiple rate cuts by the Fed in 2024, the latest forecasts suggest a more conservative approach, with one potential cut on the horizon. Fed Chair Jerome Powell’s reaffirmation of a probable cut underscores the Fed’s commitment to stabilizing inflation. However, the timing of this adjustment hinges on forthcoming economic indicators.

Inventory Is Increasing

Recent data on inventory signals a welcomed uptick in available homes especially when compared this time a year ago. This surge in inventory translates into a plethora of choices for both homeowners seeking upgrades and prospective buyers eyeing entry-level properties. For first-time buyers particularly, increased options alleviate some of the affordability concerns exacerbated by fluctuating mortgage rates. Simultaneously, current homeowners looking to sell find themselves in a favorable position, with heightened demand and an array of properties to explore.

Home Values Are Expected to Continue Appreciating

The continued increase in the value of homes underscores the allure of owning a home as an investment. Unlike renting, homeownership offers the dual benefits of shelter and equity accumulation. As the housing market continues its upward trajectory, homeowners stand to bolster their financial portfolios through accrued equity. Projections from the Home Price Expectations Survey paint a promising picture of sustained growth in home values over the coming years. This steady appreciation not only solidifies homeowners’ positions but also presents a compelling case for prospective buyers weighing their options. By capitalizing on the potential for long-term wealth accumulation, homeowners can leverage their equity to unlock new avenues of financial stability.

Opportunities in the Spring Market

The spring market offers a wealth of opportunities for both homeowners and homebuyers alike. With mortgage rates poised for potential adjustments later this year, it is estimated that 5 million buyers will enter the market for every 1% drop in mortgage rates. Coupled with the expanding inventory landscape, now is the time to stay informed and consider strategic financial decisions. Whether you’re looking to upgrade your current home or embark on the journey of homeownership, reach out today and lets discuss the opportunities for you this spring.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

After surging higher in early April, mortgage rates have moved lower in the last week.

Mortgage rates trended lower week-over-week after the Fed’s announcement of tapering their balance sheet reduction and a weaker BLS Jobs Report.

The financial markets now expect just one rate cut this year due to the persistence of elevated inflation.

The Fed Meeting

The Fed wrapped up its third of eight annual meetings yesterday that followed with its usual press conference.

The financial markets tune in to the press conference where Fed Chair, Jerome Powell, acknowledged that elevated inflation meant a delay for the Fed’s next move with rates.

The good news was Powell reiterated that the next move is more likely to be a cut rather than a hike as the Fed believes they are still on track to return inflation back to their 2% target.

BLS Jobs Report

April’s job growth missed estimates, as there were 175K new jobs created versus the 243K that were expected.

Revisions to the data for February and March also shaved 22K jobs from those months combined while the unemployment rate rose to 3.9%.

Overall, the data suggests softening in the labor sector, which could pressure the Fed to cut rates if this trend continues.

RATES MOVE LOWER AFTER FED MEETING – Positive momentum following the Fed meeting continue for a second day after Fed acknowledges next move will likely be a rate cut. https://www.mortgagenewsdaily.com/…

ACTIVE INVENTORY IS UP – Report shows that active inventory and new listings are up on both a year-over-year and week-over-week basis. https://www.calculatedriskblog.com/…

FED MEETING HIGHLIGHTS – The Fed keeps rates unchanged as it notes lack of further progress on inflation, but did acknowledge its next move would likely be a cut later in the year. https://www.cnbc.com/…

FHFA’S EQUITABLE HOUSING PLANS – FHFA announced their finalized plans to address barriers to sustainable housing opportunities for first-time and low-and-moderate income buyers. https://www.housingwire.com/…

With the recent changes in the real estate world, we believe it is more important than ever for lenders and agents to work closer together to best serve buyers and sellers. Your ability to provide value-added services to your clients not only sets you apart but also strengthens your position in the market. That’s why we have enhanced our +BuyerBenefit program with the goal of providing you with more resources for helping clients. Below are some highlights of how our +BuyerBenefit will help you:

Empower Your Listings with Strategic Financing

Our +BuyerBenefit Strategic Financing Partnership Program empowers you to market special financing incentives on your listings using both physical and digital materials. Imagine being able to offer additional value to your clients through personalized mortgage rates and financing strategies tailored to their needs.

Capture Leads and Close Deals Faster

With our program, you can capture leads effortlessly using personalized co-branded marketing tools. Plus, our lead management systems ensure that you qualify leads efficiently with your preferred lending team, paving the way for quicker closings and more transactions.

Unveil Exclusive Savings for Your Clients

One of the standout features of +BuyerBenefit is the opportunity to offer your clients exclusive savings. Eligible clients can enjoy 0.5% savings on the loan amount towards interest rate pricing, further sweetening the deal and solidifying their satisfaction. Some restrictions apply, see full terms and conditions at homeseedloans.com/buyer-benefit.

Access Cutting-Edge Digital Tools

We provide a suite of digital tools, including custom live-rates flyers for your listings and a co-branded mobile mortgage app. These tools enable prospective buyers to run personalized scenarios and explore rate buydown strategies, fostering meaningful conversations and driving conversions.

Elevate Your Marketing Efforts

From exterior marketing materials like sign riders and yard signs to interior resources like our +BuyerBenefit Book and raffle flyers, we equip you with everything you need to attract more buyers and convert leads effectively.

Seamlessly Collaborate with Your Preferred Lending Team

Our program isn’t just about providing resources; it’s about fostering strong partnerships. That’s why we offer detailed partner reports to keep you informed about the status of every active lead and loan. Additionally, our “Meet Your Preferred Lending Team” flyer simplifies the introduction process, ensuring smooth collaboration every step of the way.

Reach out today to learn more about +BuyerBenefit!

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are flat but volatile week-over-week after surging much higher the week prior.

The pressure for higher rates was caused by a strong jobs report, more troubling inflation data, and a higher consumer spending.

The odds for the first rate cut by the Fed’s July meeting has now fallen below 50%.

Consumer Price Index (CPI)

The monthly report showed inflation was much hotter than expected in March, continuing a trend we’ve seen in recent months.

Rising energy, automobile insurance, and shelter costs were the main contributors to the increase in inflation.

Annual inflation still remains below the peaks in 2022, but stubbornly high inflation readings will likely delay the Fed’s timing for rate cuts this year.

Home Builder Sentiment

The most recent Home Builder Sentiment report by NAHB showed that sentiment among builders remains in positive territory.

Internal components of the report show that buyer traffic and current sales expectations ticked higher.

Forward looking sales expectations have softened a bit due to higher rates as some buyers remain on the fence.

MORTGAGE RATES FLAT – Rates are relatively unchanged week-over-week but the daily changes have been volatile. https://www.mortgagenewsdaily.com/…

RATE CUTS DELAYED – The Fed Funds Rate could stay higher for longer if inflation persists. https://www.morningstar.com/…

WHAT HOMEBUYERS WANT – A recent study shows that a vast majority of homebuyers are looking for a home with at least one home office. https://www.eyeonhousing.org/…

HOME PRICES KEEP CLIMBING – Higher rates are keeping a lid on housing supply and putting pressure on home price appreciation. https://www.housingwire.com/…

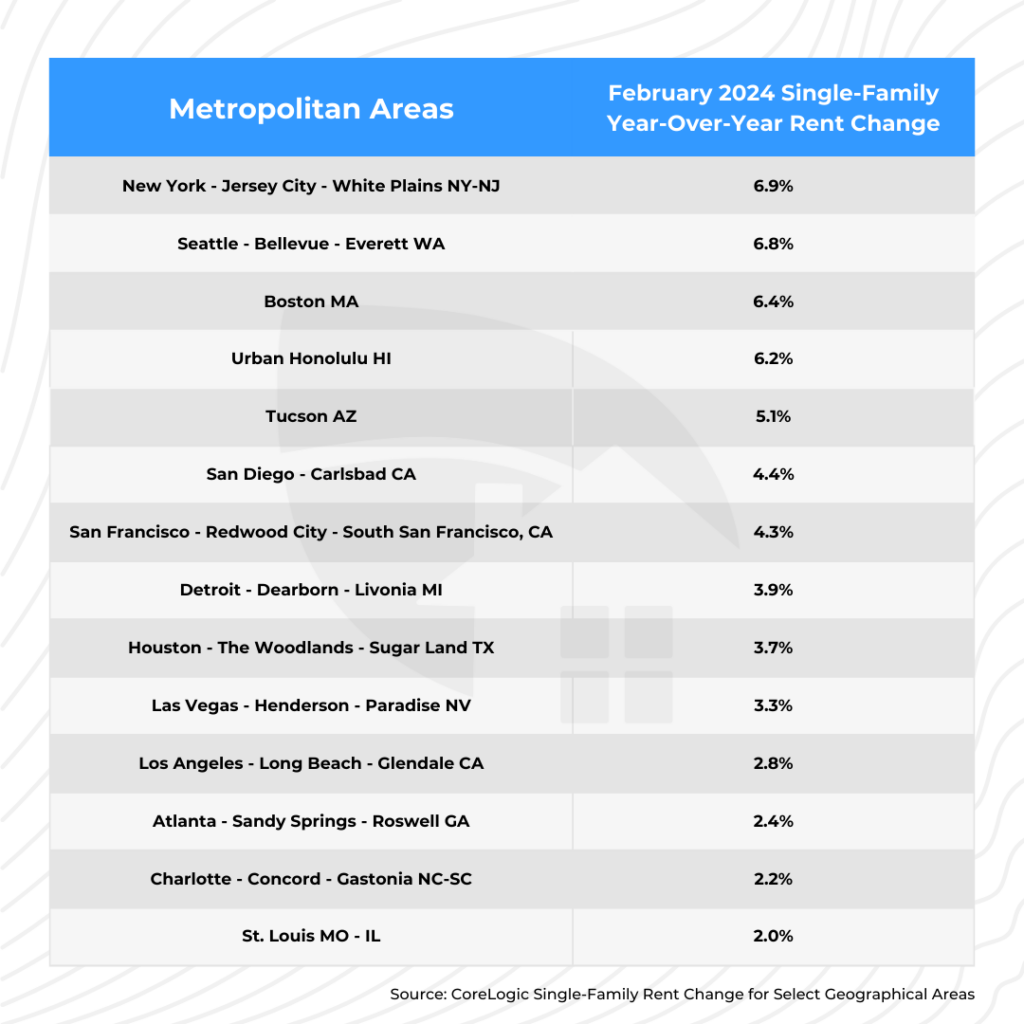

In recent years, the rental market has seen a significant trend: rent prices are steadily climbing year after year. According to a recent CoreLogic Index for US Single-Family Rent, February 2024 marked the highest annual increase in the last 10 months, with US single-family rents surging by 3.4% year-over-year. Many large cities, in particular, have witnessed spikes of over 5%, putting a strain on renters’ budgets as they also grapple with high inflation.

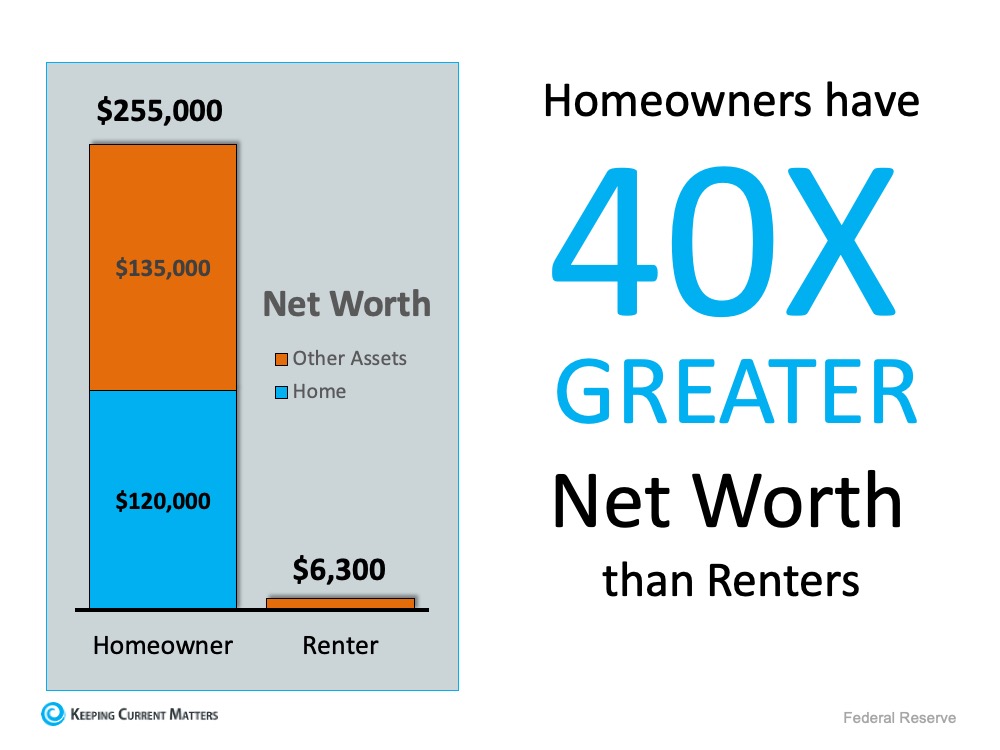

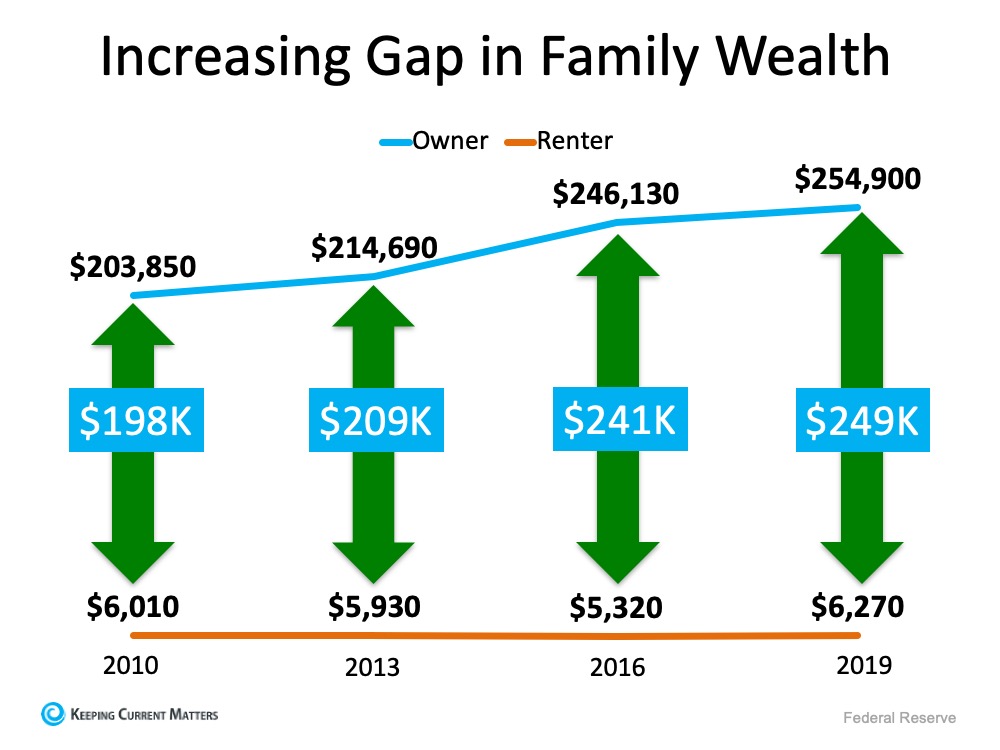

As rent prices continue to soar, many individuals and families are grappling with the question of whether renting or owning a home is the better financial choice. The answer becomes increasingly clear when considering the broader economic landscape and the long-term benefits of homeownership. In fact, data from the Federal Reserve reveals that the median net worth of homeowners is a staggering 40 times greater than that of renters.

Benefits of Owning A Home

Owning a home provides stability and predictability in housing expenses. Unlike renting, where landlords can raise rents at their discretion, homeowners enjoy fixed monthly payments, consisting of principal and interest, that do not fluctuate over time. This stability not only offers peace of mind but also serves as a hedge against inflation, as the cost of housing remains consistent regardless of economic conditions.

Homeownership enables individuals to build equity over time and leverage their asset. Home prices have historically appreciated, increasing in value in 74 out of the last 82 years. Additionally, as mortgage payments are made, homeowners accumulate equity in their property, which can then be tapped into for various purposes, such as funding home improvements, financing education, or even investing in additional real estate properties. This ability to leverage one’s home as an assets opens up a world of financial opportunities and contributes to long-term wealth accumulation.

In conclusion, as rent prices continue to rise annually, the case for homeownership as a superior investment becomes increasingly compelling. Not only does homeownership offer the potential for significant wealth accumulation, but it also provides stability, predictability, and the opportunity to leverage one’s assets for further financial growth. Aspiring homeowners should consider these factors carefully when making their housing decisions, as owning a home represents not only a roof over one’s head but also a pathway to financial security and prosperity.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates increased noticeably on Monday and are higher on a week-over-week basis.

The increase in rates was due to higher than expected numbers for the S&P and ISM manufacturing indices, which also mentioned higher prices in their reports.

Prices are crucial due to the persistent inflationary pressures, and if they fail to revert to the downward trend it will make it hard for the Fed to want to cut rates.

Personal Consumption Expenditures (PCE)

This is the Fed’s preferred measure of inflation and its goal is for the Core reading, which strips out volatile food and energy prices, to be at 2%.

Last week’s release of data showed that the Core headline reading fell to 2.8%, but the progress lower has been slowing.

With future data projecting a slow progress towards 2% for Core PCE, it may take weaker labor market data before the Fed cuts rates.

BLS Jobs Report

March’s job growth roared in above forecasts, as the BLS reported that 303K new jobs were created.

68% of the job gains came from three sectors: Leisure & Hospitality (49,000), Government (71,000), and Education & Health Services (88,000)

Revisions to the data for January and February added an additional 22K jobs to those months combined.

Unemployment rate declined to 3.8%.

Case-Shiller Home Price Index

The Case-Shiller Home Price Index, which is considered the “gold standard” for appreciation, showed home prices rose 6% year-over-year in its most recent report for January 2024.

The 6% annual rate is the fastest increase since 2022 and all 20 cities in its composite index saw annual increases for the second straight month.

Home values are expected to remain supported throughout 2024 as housing demand remains high.

RATES MOVE HIGHER EARLY IN WEEK – The concern for higher prices and inflation after Monday’s manufacturing data pushed rates higher early in the week. https://www.mortgagenewsdaily.com/…

ISM INDEX TURNS POSITIVE – A barometer of business conditions at U.S. manufacturers turned positive in March for the first time in 17 months. https://www.marketwatch.com/…

BABY BOOMERS PLAN TO STAY IN HOMES – More than three-quarters of baby boomers plan to stay in their home as they grow older. https://www.businesswire.com/…

HOUSING MARKET STAYS TIGHT – New home listings are down to start the Spring market, but competition remains fierce as demand is still high. https://www.mpamag.com/…

You can read our previous blog post on trigger leads and how to reduce them by CLICKING HERE.

In the world of mortgage lending, trigger leads have long been a point of contention. While some praise them for their potential to foster competition and secure better rates for applicants, most oppose them for inundating borrowers with unwanted solicitations. However, developments in regulations over the past few years are refining rules for trigger leads in the pursuit of stronger data privacy and consumer protections. Most recently, the FCC announced a new ruling on December 13, 2023 that will effectively close the “lead generator loophole.”

The FCC’s adopted rule to close the lead generator loophole marks a significant change in the way consumer information is shared with businesses through comparison shopping websites. Under this rule, consumers must provide individual consent for their information to be shared with each business, effectively closing the loophole that allowed for the sale of a single lead to multiple businesses at once. This move aims to address consumer frustrations with receiving an overwhelming number of calls and texts after submitting an online lead.

How Will This Ruling Impact Borrowers and Businesses?

Mortgage applicants can expect relief from the inundation of solicitation calls. The previous influx of unwanted calls and texts from solicitors has been a source of frustration for many applicants, but the FCC’s actions aim to mitigate this issue, ultimately enhancing the borrower experience.

Requiring businesses to obtain one-to-one consent before contacting new leads. The rule will likely reshape lead strategies for businesses built on this type of lead generation model and challenge the operational models of comparison-shopping sites due to compliance regulations.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Last week’s comments on rate projections by the Fed Chair, Jerome Powell, retained the Fed’s previous expectation of 3 rate cuts by the end of this year and gave the forward-looking markets something to be hopeful for, which led to a decrease in mortgage rates.

The labor market has been showing signs of weakness with the unemployment rate ticking up.

Inflation Higher Than Expected

Recent inflation data for both the Consumer Price Index (CPI) and Producer Price Index (PPI) came in higher than expected.

The month-over-month changes of 0.4% in CPI and 0.3% in PPI imply an annualized reading of 4.8% and 3.6%, respectively (the Fed’s target is 2% for core readings).

Inflation is the biggest concern for interest rates, so it was no surprise to see the Fed unwilling to cut rates just yet.

March Fed Meeting

The Fed left rates unchanged following their meeting that concluded today for the fifth straight time, but did acknowledge the recent higher inflation readings could be a result of seasonality that was impacting the data.

Federal Reserve Chair Jerome Powell stated that any adjustments to the policy rate would depend on incoming data and the evolving economic outlook.

The Fed’s dot plot showed they expect to cut rates three times in 2024 with the Fed Funds Rate decreasing to 4.6%.

RATES IMPROVE AFTER FED MEETING – Mortgage rates have trended higher over the last week due to inflation reports, but comments by Jerome Powell did help ease concerns. https://www.mortgagenewsdaily.com/…

FED HOLDS RATES STEADY – The Fed maintained its Fed Funds Rate following its two-day policy meeting as expected, and provided their thoughts on the recent inflation readings. https://www.cnbc.com/…

BUYERS’ DESIRED HOME SIZES – A NAHB study shows that buyers want smaller sized homes than they did 20 years ago. https://www.eyeonhousing.org/…

NAR SETTLEMENT MYTHS – Debunking some of the myths from the recent NAR settlement agreement. https://www.housingwire.com/…

Just as you would want a listing agent to help you maximize the sale of your home, navigating the intricate world of real estate demands the guidance of a buyer’s agent. After all, purchasing a home stands as one of the most significant financial decisions one can make. Amidst the myriad of decisions, paperwork, and negotiations, having trusted and knowledgeable professionals by your side can make all the difference in helping you avoid costly mistakes and missed opportunities. In this blog post, we’ll delve into the crucial role of a buyers agent in the home buying process and explore how their collaboration with mortgage lenders ensures a smooth and informed journey towards homeownership.

Expertise & Knowledge

One of the standout advantages of having a buyer’s agent by your side is their profound understanding of the local real estate market. They know the ins and outs of neighborhoods, property values, and current market trends. Additionally, they offer valuable insights into what it means to be a homeowner and provide education on topics such as insurance and utilities, ensuring you’re well-informed every step of the way.

Guidance & Support

Buyer’s agents are more than just property tour guides. They serve as trusted advisors, listening to your needs and preferences and assisting you in finding the perfect home. From scheduling viewings to gaining access to properties, they handle the logistics, making the process smoother and more efficient.

Negotiation & Advocacy

When it comes to negotiations, buyer’s agents are your advocates. With your best interests in mind, they navigate the intricacies of the negotiation process, ensuring you secure the best possible deal. Their keen eye for detail allows them to evaluate the value of a home relative to the local market, spot potential issues on the property, and advocate for necessary repairs or adjustments.

Example: Jon and Jane finally found a home they loved and were willing to offer $25,000 over the asking price. Their agent, however, suggested they only offer the asking price after performing a comparative market analysis (CMA) that calculates a home’s value based on the recent sales of similar real estate in the area. In the end, the sellers accepted Jon and Jane’s offer at the asking price and saved them the additional amount they were willing to include.

Orchestrating The Transaction

Buying a home involves a multitude of moving parts, from putting together the offer to coordinating with lenders and sellers. Buyer’s agents serve as conductors, guiding you through each stage of the transaction with clarity and expertise. They demystify the home buying process, ensuring you understand every document and decision along the way.

In conclusion, the significance of having a buyer’s agent in the home buying process cannot be overstated. Their expertise, guidance, and advocacy are invaluable assets, particularly when making such a substantial financial decision. As you embark on your home buying journey, remember the importance of seeking professional assistance. Together with Homeseed as your lender, we will work to ensure your home buying experience is seamless, informed, and ultimately, rewarding.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are lower week-over-week after the recent PCE inflation data came in as expected.

Downward momentum on rates continued as yesterday’s ISM Services index showed a big decline in prices paid for the service sector where we are seeing most of the inflation.

Tomorrow’s BLS Jobs Report is potentially a market mover as recent comments by Fed members show they are paying close attention to the labor market.

Personal Consumption Expenditures

Fed’s favorite measure of inflation, Personal Consumption Expenditures, showed the headline or all-in inflation declined from 2.6% to 2.4% year-over-year.

Annualizing the last 6-months of core readings, which the Fed says they are looking at, puts Core PCE at 2.46% and close to their 2% target.

There are emerging signs that the consumer is coming under pressure when looking at income and spending data.

CoreLogic Home Price Insights

Home prices were up 5.8% year-over-year in January, which is an increase from 5.5% on the previous report.

Forecasts for February show home prices being flat and will rise by 2.6% over the next 12 months, but it is worth noting that CoreLogic has been very conservative in the past.

Despite fewer buyers in the current market, housing demand still exceeds available inventory which is why home prices remain supported.

RATES LOWER AHEAD OF JOBS REPORT – Recent inflation data helps mortgage rates move lower ahead of the important BLS Jobs Report. https://www.mortgagenewsdaily.com/…

FEBRUARY LAYOFF NUMBERS – Layoff announcements in February hit their highest level for the month since the global financial crisis in 2009. https://www.cnbc.com/…

HOME-SELLING SENTIMENT MOVES HIGHER – February data shows more consumers believe it is a good time to sell a home ahead of the spring homebuying season when compared to January. https://www.fanniemae.com/…

CREDIT SCORES WORSEN – For the first time in a decade, the average credit score for consumers fell according to FICO. https://www.investopedia.com/…

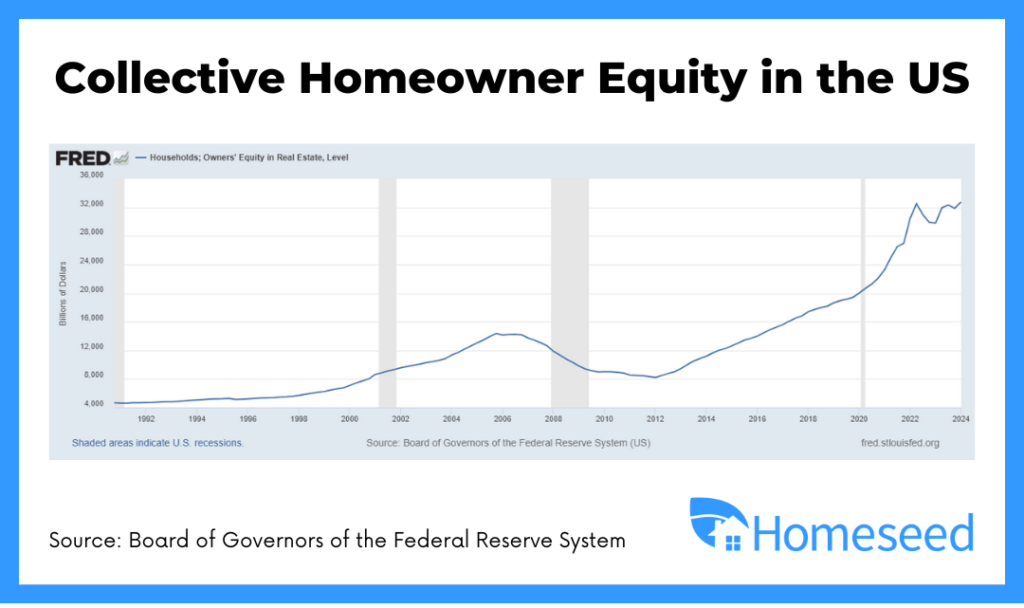

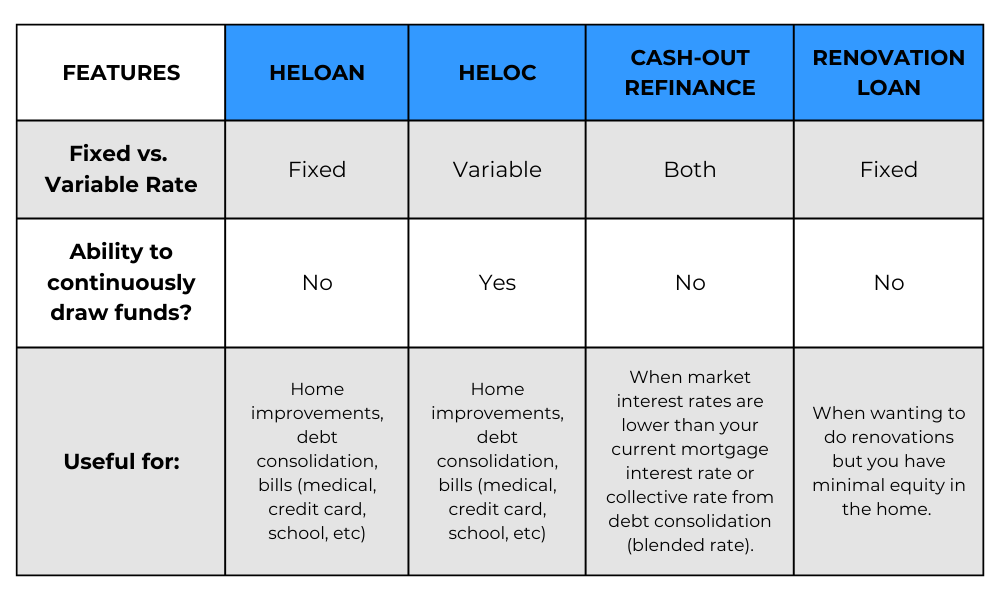

Homeownership brings with it a valuable asset beyond the comfort of having a place to call your own – home equity. Today, homeowners collectively hold trillions in equity, presenting an opportunity to leverage these funds for various financial opportunities. Whether it’s funding home renovations, consolidating debt, making financial investments, or covering life events, your home equity can be a valuable resource to leverage for your benefit. In this blog, we’ll discuss the many options you have available to access your equity!

Loan Products to Access Your Equity:

Home Equity Loan (HELOAN):

A fixed-rate loan offering a lump sum payment.Ideal for those with a clear vision of their financial needs.

Consistent monthly payments, providing stability.

Home Equity Line of Credit (HELOC):

A flexible credit line secured by your home’s equity.Allows for periodic access to funds when needed.

Adjustable interest rates, providing flexibility but requiring careful financial planning.

Cash-out Refinance:

Replace your existing mortgage with a new one, withdrawing excess funds.Fixed monthly payments and potential for lower interest rates.

Suitable for those looking to streamline mortgage payments and access substantial funds.

Renovation Loan Highlights:

Borrowing Based on Expected Home Value:

Allows you to access funds based on the anticipated post-renovation value of your home.

A great solution for those seeking additional funds for renovation but lacking sufficient equity in the home.

Building an Accessory Dwelling Unit (ADU):

Utilize renovation loans to finance the construction of an ADU.

Enhances the property’s value and provides potential rental income.

Purchasing a Property That Needs Upgrades:

The renovation loan product can also be used on a home purchase.

The downpayment can be as little as 3% with a HomeStyle renovation loan.

What Loan Product Is Best:

When deciding to access your home equity, it’s crucial to consider various factors that can significantly influence which loan product is best for your situation. Two key considerations are the amount of debt you are borrowing and the interest rate of the loan product. As your loan advisor, we help provide a blended interest rate calculation that takes into account the interest rates associated with your existing mortgage and the new loan you’re considering, weighted by the loan amounts. This helps you assess the potential impact of blended interest rates on your financial situation, providing clarity on the short-term and long-term implications of each loan option.

As you explore possibilities with your home equity, remember that your homeownership is not just a place to live but a gateway to financial opportunities. Now is the time to leverage your home equity and unlock its potential. Our dedicated team is here to guide you through the process, offering insights, expertise, and personalized solutions. Whether you’re considering a HELOAN, HELOC, or renovation loans, our goal is to empower you to make informed decisions as a homeowner.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

The main reason for higher mortgage rates this week was due to a weak 20-year bond auction that caused a sell off in the bond market.

Mortgage rates have seen a slight upward trend since the beginning of the year due to stronger inflation and labor market data.

The minutes from the most recent Fed meeting were released this week which confirmed that they are certain to cut rates this year, but this will likely not occur by the next meeting in March.

Existing Home Sales

Housing inventory remains low with about 3 months of supply of homes versus the normal market value of 4.6 months.

The median home price rose by 5% from the previous year, reaching $379,100.

Lawrence Yun, Chief Economist for NAR, notes that mid-priced homes are receiving multiple offers, with a significant share (32%) being cash deals, indicating a market driven by record-high housing wealth.

Producer Price Index

The Producer Price Index measures inflation from the perspective of producers.

Similar to the recent CPI report, inflation on the producer side was also higher than expected for the month of January.

Services were the main culprit in the high inflation reading that includes items such as health care and legal services.

RATES MOVE SLIGHTLY HIGHER – A weak 20-year bond auction pushes rates slightly up to highs not seen since November. https://www.mortgagenewsdaily.com/…

FHA HELPING BORROWERS KEEP HOMES – The new offering, called the Payment Supplement, will help borrowers bring their mortgage payments current and avoid foreclosure. https://www.hud.gov/…

ACTIVE INVENTORY IS UP – Recent data shows that active inventory is up 15.7% and new listings are up 0.9% YoY. https://www.calculatedriskblog.com/…

THE FED EXPRESSES CAUTION – Meeting minutes show that the Fed plans to cut rates this year, but express caution in lowering too quickly. https://www.cnbc.com/…

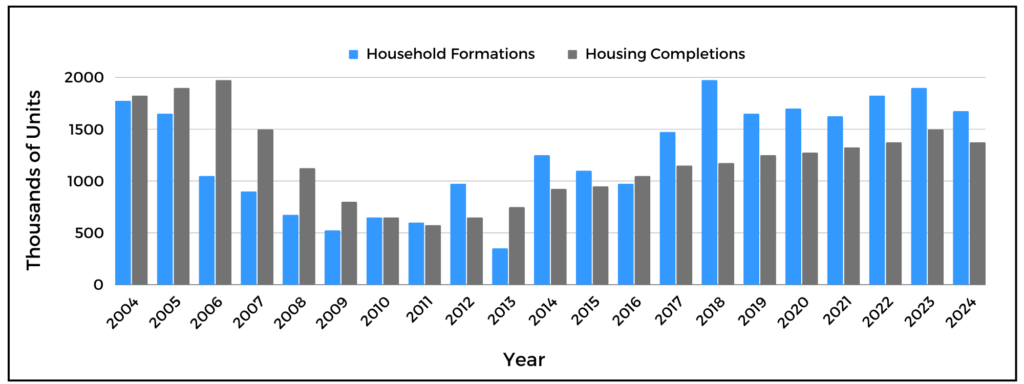

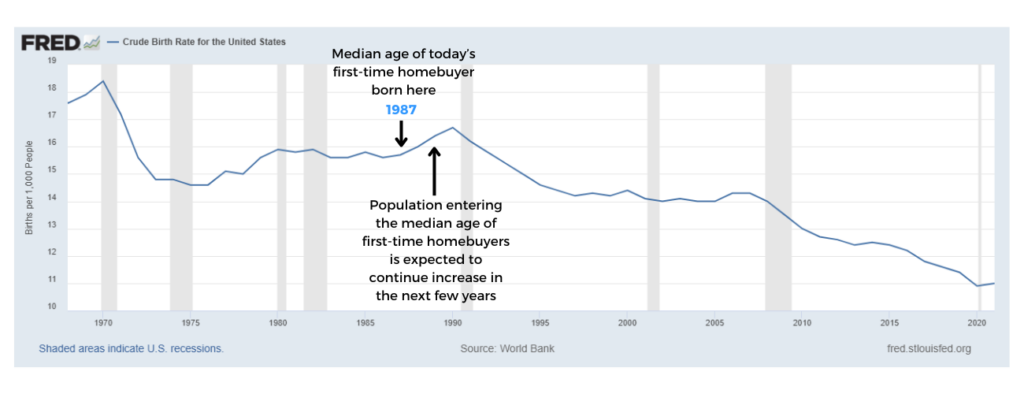

In today’s dynamic real estate landscape, a persistent housing inventory shortage defines the market’s competitiveness. This scarcity arises from two main factors. Firstly, household formations consistently outpace housing completions over the past decade, with projections indicating a continued trend. The growing population entering the median age of first-time home buyers (37 years old) further exacerbates this issue. Secondly, many homeowners are hesitant to sell due to the current higher interest rate environment. While they might have considered upgrading in the past, prevailing higher interest rates anchor them to their current residences. This dual dynamic, driven by increasing household formations and homeowners holding onto their properties, shapes the current sellers market and intensifies competition.

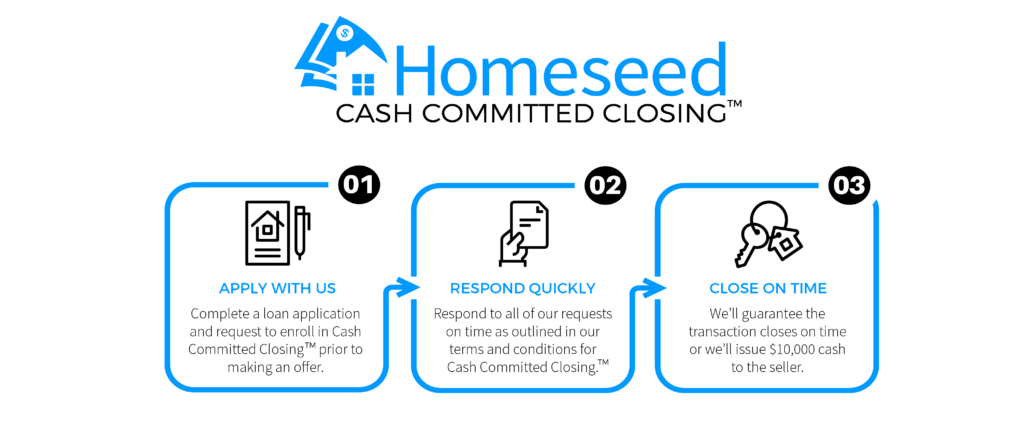

Making Your Financing as Competitive as Possible in the Seller Market

Where time is of the essence, the importance of offering a quick closing cannot be overstated. Enter Homeseed’s Cash Committed Program, a highly impactful tool in the homebuying process. Unlike traditional pre-approvals, this program provides an underwritten credit approval that signifies a more robust evaluation of your application and commitment to financing. The added assurance of a $10,000 guarantee for closing on time not only expedites the process but also builds trust with sellers, making your offer stand out in multiple offer situations.

Homeseed also offers a Buy Before You Sell Program that allows homebuyers to move quickly on the purchase of the new home rather than worrying about selling their current residence. This strengthens their offer on a new property as they are not contingent on the sale of their current home. Buy Before You Sell also offers the option to receive a bridge loan to help cover the down payment on the new purchase or to make repairs to the departing residence.

Create Your Inventory and Build the Home of Your Dreams

With inventory at an all-time low, homebuyers have also expressed a need to find alternative avenues for homeownership. Building a new home or rehabilitating an existing one emerges as a strategic move. These options often come with the enticing prospect of instant equity post-construction or rehab, where the appraised value exceeds the initial investment. Moreover, with low down payment options, such as 5% with conventional financing or 3.5% with FHA financing, these programs make homeownership more accessible.

It’s essential for homebuyers to adapt and thrive in this competitive market, and a crucial aspect of this is collaborating with a local lender who understands the nuances of the market. Working with someone knowledgeable about the local real estate landscape can provide invaluable insights and pave the way for a smoother and more successful homebuying journey. As you embark on your homebuying journey, consider exploring innovative financing options with Homeseed. The dynamic nature of the real estate market calls for proactive and informed decisions, and Homeseed is here to empower you on your path to homeownership.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are higher this week as a result of strong labor market and manufacturing data.

The BLS Jobs Report showed nearly double the amount of jobs were added to the market than expected.

The ISM Non-Manufacturing PMI was also higher than expected and the upbeat economic data put additional upward pressure on rates.

BLS Jobs Report

The report for January showed that the 353,000 jobs created were nearly double the expected 180,000.

One thing to be mindful of is that January is a month of heavy adjustments due to new benchmarks, seasonal adjustments, and population controls.

Despite the job gains, the entire labor force is working on average 30 minutes less per week, which is equivalent to 2.4M jobs lost.

We will have to wait for February data to see if the labor market tightening once again.

Home Values Continue to Appreciate

The two most notable housing indices, Case-Shiller and FHFA, both recently released data showing that home prices set new highs.

Although data for December 2023 is not available yet, both indices show that home values were on pace to appreciate by 6% in 2023.

Lower numbers for existing inventory and active listings will continue to be supportive of home prices throughout 2024.

MEDIA SAYING HOUSING CRASH – But housing credit data today looks nothing like what was seen in 2008. https://www.housingwire.com/…

BOOST TO HOUSING SENTIMENT – The Fannie Mae Home Purchase Sentiment Index reached its highest level in nearly two years. https://www.fanniemae.com/…

TWO SIDES TO JOB MARKET – Economists and reports say the labor market is strong, but job seekers don’t share the same confidence. https://www.cnbc.com/…

Homeownership has long been considered a cornerstone of the American dream, providing not only a sense of stability and security but also a unique avenue for building wealth. For many, purchasing a home is not just about having a place to call their own; it’s a strategic financial move that can lead to long-term prosperity. Below we’ll provide a decade-by-decade analysis on home values and explore how homeownership is a powerful investment tool, enabling individuals to leverage their assets and capitalize on the appreciation of real estate.

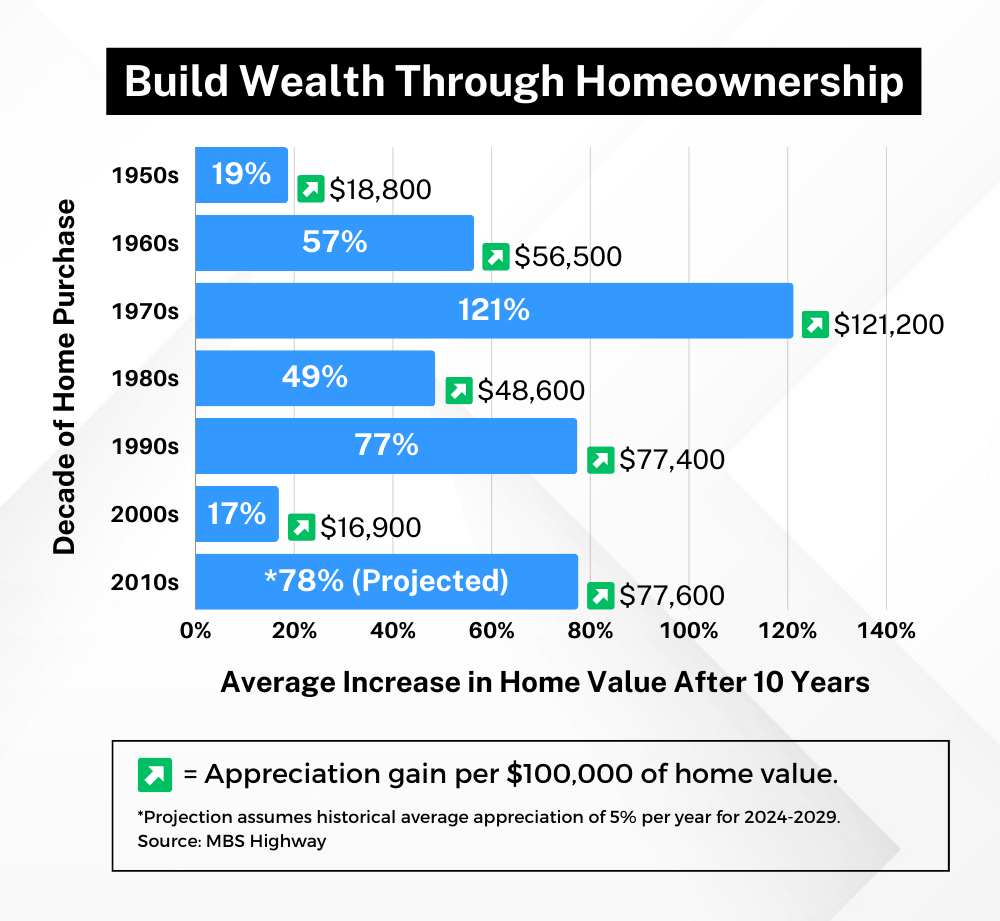

Historical Appreciation By The Decade

Consistent Appreciation: Regardless of the decade, those who invested in homeownership and held onto their properties for 10 years experienced positive appreciation on average. This consistency underscores the enduring nature of real estate as a wealth-building asset.

Diversification of Investments: The data highlights how real estate can serve as a valuable diversification tool for investment portfolios. While other assets may experience volatility, real estate has historically shown a trend of appreciation over time.

The Power of Leverage in Real Estate

One of the unique aspects of real estate investment is the ability to use leverage. When you purchase a home, you typically make a down payment (an initial investment) while borrowing the rest through a mortgage. This means you control an asset’s full value with a relatively small upfront payment. As the property appreciates, the return on your investment is calculated based on the property’s entire value, not just your down payment. This leverage magnifies the potential for wealth accumulation.

Homeseed Can Help You Get Started

Discover the possibilities with our exclusive loan programs that offer little to no down payment options. This means you can potentially start building equity and wealth with very little upfront investment. Our commitment is to make homeownership accessible and financially advantageous for you. Contact us today to discuss your goals, explore available opportunities, and make informed decisions about your real estate investment. Your path to homeownership and financial prosperity starts with a conversation. Let’s connect and turn your homeownership dreams into reality!

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are relatively unchanged week-over-week with some volatility mixed in due to economic data and bond auction results.

Last week saw 2-year, 5-year, and 7-year Treasury auctions that were met with weak demand and put upward pressure on mortgage rates.

Recent GDP and labor market reports came in stronger than expected and the Fed would like to see more economic weakness to support disinflation.

Personal Consumption Expenditures (PCE)

Headline inflation rose 0.17% in January, close to the expected 0.2%, while the year-over-year reading remained at 2.6%.

Annualized core PCE over the last 6 and 8 months is 1.85% and 2.08%, respectively, which are close to the Fed’s target of 2%.

Although the Fed prefers the Core PCE measure for gauging inflation, it should be noted that the CPI tends to move the markets a bit more.

Pending Home Sales

Pending Home Sales (signed contracts on existing homes) surged 8.3% from November to December.

The large jump was attributed to the decline in mortgage rates we’ve seen since the highs back in October 2023.

The Chief Economist at the National Association of Realtors, Lawrence Yun, noted that sales are expected to rise significantly in each of the next two years.

An increase in the supply of homes on the market will be essential to satisfying all of the demand that current exists.

RATES UNCHANGED WEEK-OVER-WEEK – Mortgage rates were volatile within a narrow range over the last week but are relatively unchanged. https://www.mortgagenewsdaily.com/…

ECONOMY BOOSTED BY NEW HOME SALES – Continue demand for new housing helped employ workers, stimulate the purchase of goods, and avoid a recession in 2023. https://www.housingwire.com/…

ACTIVE INVENTORY RISES – For the 11th straight week, active listings grew and looks to improve availability and affordability heading into the spring season. https://www.calculatedriskblog.com/…

INFLATION CONTINUING TO COOL – The recent PCE report showed inflation continuing to cool and near the Fed’s 2% target. https://www.cnbc.com/…

At some point in our lives, we’ve all pondered the age-old question: when is the ideal moment to embark on the journey of homeownership? This decision is often influenced by personal finances and life circumstances. Fortunately, for those with the desire and means, the current market offers an advantageous time to make the move into homeownership. Despite some headwinds like rising home prices and higher interest rates, the numerous benefits of purchasing now far outweigh these obstacles.

An Investment to Build Wealth:

Owning a home builds equity, but that takes time for the asset to grow. The earlier you can start the better. Remember, time in the market beats trying to time the market.

Mortgage payments contribute to your ownership stake, unlike rent payments that go into your landlord’s pocket.

In the future, your home equity becomes a powerful financial tool to be leveraged for other investments or major life expenses.

Property values historically trend upward, providing you one of the safest investments you can make.

Homeowners enjoy tax incentives, with tax-deductible mortgage interest payments.

An Opportunistic Time to Purchase Now:

Forecasts indicate an expected decline in mortgage rates in 2024, which will likely increase affordability and heighten competition on the limited supply of homes.

Purchasing now grants an advantage ahead of the projected surge in competition, while allowing you to capitalize on equity gains and refinance opportunities once rates drop.

The higher loan limits for 2024 contribute to an increase in affordability for you, especially in the earlier part of the year as home prices are expected to continue rising throughout 2024.

Homeseed’s Programs & Strategies for First-Time Homebuyers

Down Payment Assistance Programs: Programs designed to aid with down payment and closing costs, providing valuable financial support to ease the initial financial burden of purchasing a home.

Zero Down Payment Loans: Loan programs requiring no down payment, particularly beneficial for veterans (VA) or those residing in rural areas (USDA).

First-Time Homebuyer Programs: Loan programs with lower down payments and improved rates that are created for low- to moderate-income first-time homebuyers.

Seller Concessions: We offer financing strategies where the seller can help provide additional assistance to reduce the cash you need to close.

Choosing homeownership over renting is a strategic move that goes beyond the immediate advantages of financial investment. It’s a commitment to building wealth and securing long-term benefits for you and your family. With Homeseed’s support and specialized programs for first-time buyers, the path to homeownership becomes even more attainable. Take the next step with Homeseed and make the move towards homeownership today.

Welcome to Homeseed’s 2024 Mortgage & Real Estate Forecast! As we enter the exciting year of 2024, the anticipation and speculation surrounding the mortgage market and housing industry have prospective homebuyers carefully watching. In just the last three years, we’ve gone from seeing all-time low mortgage rates to some of the highest mortgage rates in the last two decades due to significant global events and economic shifts. To better understand what potentially lies ahead for this year, let’s dive into a forecast for the mortgage market and housing industry in 2024.

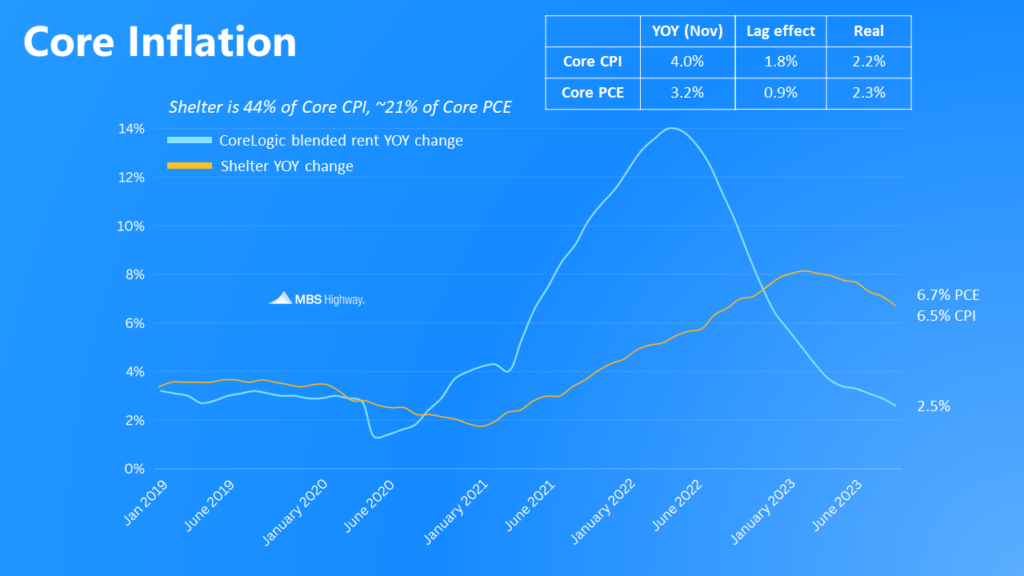

Inflation: The Driving Force for Mortgage Rates

Inflation has emerged as a pivotal factor shaping the mortgage market. After reaching a near 40-year high of 5.3% in March 2022, Core Personal Consumption Expenditures (PCE) has been on a gradual decline and now hovers at 3.2%, which is near the Federal Reserve’s (Fed) goal of 2%. Given the improvement on inflation, the Fed signaled they would begin rate cuts to their Fed Funds Rate before reaching the 2% target in hopes of easing into its inflation goal with minimal negative effects to the economy. With shelter accounting for 21% of Core PCE, CoreLogic’s most recent measure of shelter costs showed a 2.5% year-over-year increase in their real-time blended rents data. This suggests a continued improvement for inflation lies ahead as the shelter data used by the PCE report lags the real-time shelter data, and the markets are now predicting the first rate cut by the Fed as early as March 2024.

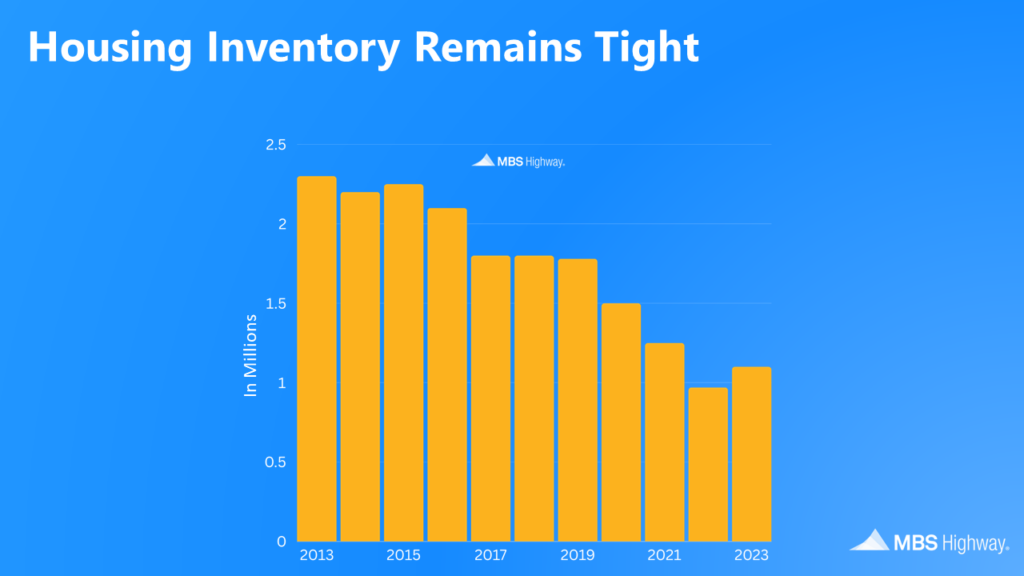

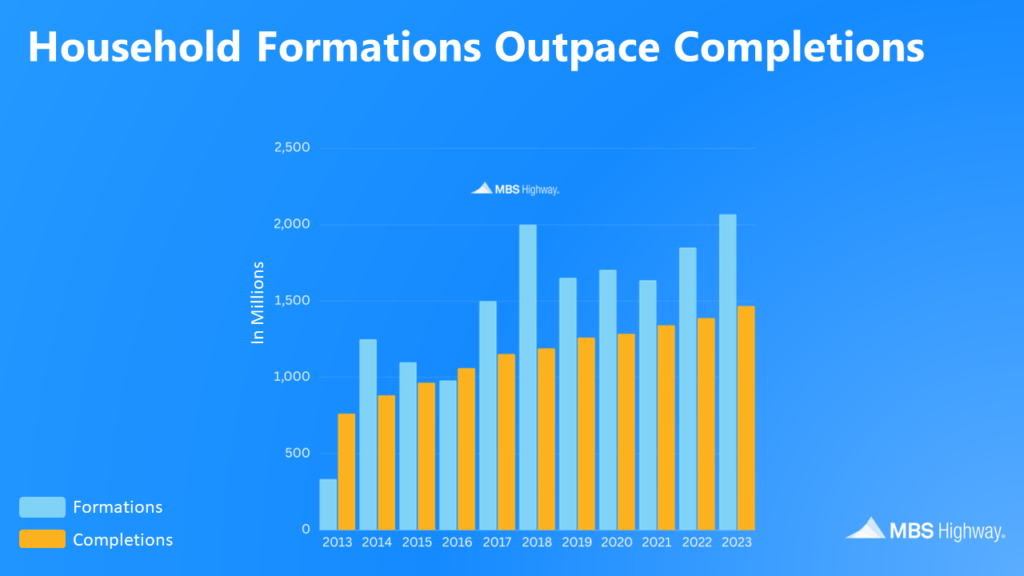

Supply and Demand: Limited Inventory Pushes Home Prices Higher

The housing market continues to grapple with enduring challenges in inventory shortage, fueling a steady increase in home prices. Despite efforts to address the housing deficit, housing starts persist below household formations, indicating a sustained scarcity of available homes for sale coming to the market that is unable to meet the escalating demand. This ongoing imbalance between the supply of homes and demand from buyers will likely intensify competition if mortgage rates continue to come down, leading to the possibility of bidding wars and soaring prices once again.

Mortgage Rate and Real Estate Forecasts

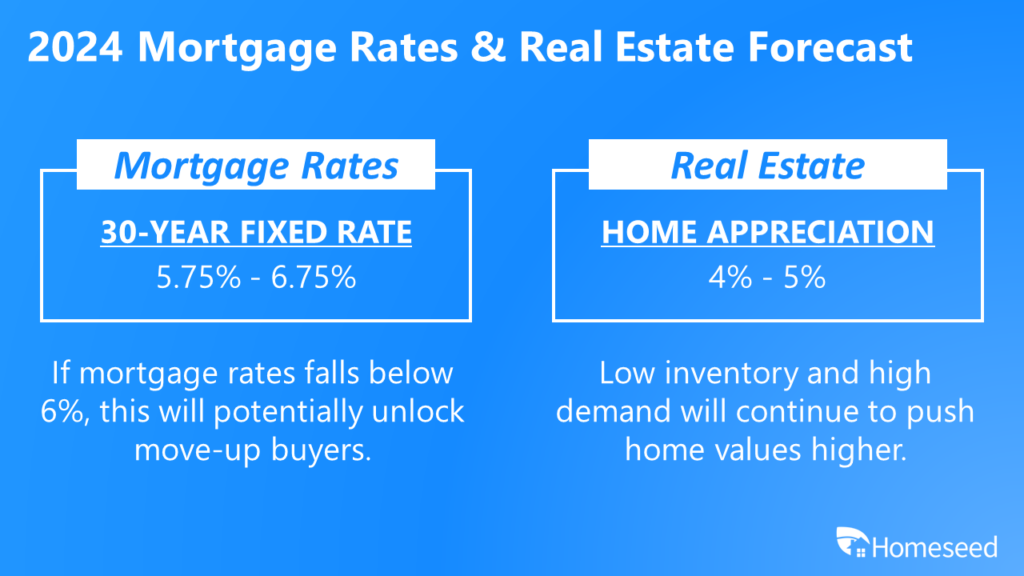

Given the trajectory of inflation, we forecast the 30-Year Fixed Rate Mortgage to fluctuate between a rate range of 5.75%-6.75% throughout 2024. If rates fall below 6%, this will potentially unlock move-up buyers who are current homeowners that want to upgrade their homes.